.png&w=384&q=75)

1. Theoretical Basis for the Digitization of Cash Operation in banking system

Cash and vault operations within commercial banks (CBs) encompass the process of organizing, controlling, and supervising all activities related to the storage, receipt, disbursement, transportation, counting, and inventory of cash and valuable assets, ensuring physical security, accounting accuracy, and legal compliance [16, p. 12-20]. According to Circular No. 01/2014/TT-NHNN, cash management tasks include delivery, safekeeping, and transportation; inspection, inventory, handover cash, precious assets, and valuable papers discrepancies in banking sector; and cash receipts and disbursements between commercial banks and the State Bank of Vietnam (SBV), credit institutions (CIs) and customers. This activity is a particular characteristic of commercial banks (CBs), demanding extremely high precision and security to ensure the smooth and safe circulation of currency, payments, and financial transactions of the economy.

Despite the increasing development of non-cash payment instruments and services in the economy, cash still accounts for 20% of the total means of payment, and the costs associated with managing, storing, and circulating cash comprises 5-10% of a bank's total expenses [7]. Currently, cash payment continues to represent 16% (USD 6 trillion) of the total global consumer payment value and remain the primary payment method in 6 out of 14 economies in the Asia-Pacific region (World Pay 2024). Therefore, the digitization of bank cash and vault operations is an essential requirement to reduce costs, enhance efficiency, improve customer experience, and foster the comprehensive digital ecosystem of banking system.

Digitization of cash and vault operations in banking system is a comprehensive restructuring process of the cash management model, based on digital technology platforms (especially Industry 4.0 technologies such as AI, RPA, Big Data, API, IOT…). This contributes to enhancing operational efficiency, minimizing risks, optimizing cash reserves, and simultaneously strengthening internal connectivity between the cash operations department and other operation departments in commercial banks (CBs); between banks and customers; and between CBs and the central bank (Gartner 2020, Von & Langerman, 2022). Technology plays a crucial role with centralized reserve management systems, automated counting devices, and demand forecasting analytical software, which collectively reduce errors and improve operation accuracy [8; 16, p. 12-20].

Digital transformation of bank cash and vault operations is not merely the application of technology to replace manual tasks, but rather a systematic reorganization process – encompassing technology, processes, people, and organizational structure – aimed at enhancing the efficiency, transparency, and adaptability of the cash and vault operations department in response to modern operation (Vial 2019). The digitization of cash and vault operations, the application of automated counting and sorting machines, IOT sensors for warehouse environment monitoring, real-time data analysis and cash demand forecasting help reduce costs and optimize capital turnover [8; 16, p. 12-20]. Digitization is an essential factor for bank cash and vault operations to transform from a manual operational center into a strategic decision, enhancing competitiveness and strengthening adaptability to a volatile global financial landscape (Hoang Anh et al., 2025).

According to a survey by Aite (2018), 86% of the 70 US banks surveyed during 2017-2018 implemented technological solutions to modernize cash and vault operations, followed by significant benefits such as increased accuracy in cash demand forecasting; enhanced competitiveness, product differentiation, satisfying customer needs, and improved customer experience. Aviva Tech (2023) evaluates that cash and vault management technology in the 2025–2030 period will be user-friendly, system-wide synchronized, capable of analysis and forecasting, and efficient in user management. Accordingly, artificial intelligence (AI) is estimated to reduce operational costs by 20–30% and increase productivity in banking operations (including cash and vault operations) by approximately 2.8%–4.7%, while boosting financial fraud detection capabilities by 30–50% (McKinsey, 2023). Concurrently, a Citi GPS survey (June 2024) indicated that 93% of banks expect AI implementation to increase profits across all global banking segments by an average of 9% during 2024-2025, with Europe and Asia showing the strongest increases at 22% and 18%, respectively. ICBC (China) and DBS (Singapore) set an example of utilizing blockchain, IOT sensors, and real-time data management systems to enhance asset monitoring capabilities and improve compliance in cash and vault operations [1; 11, p. 45-51]. The Centralized Management and Issuance of Cash (CMO) System (2011) by the SBV of Vietnam has reduced the volume of cash transactions between credit institutions and the SBV by 20% to 30%, while also enhancing security during transportation and cash replenishment, reducing operational risks in cash and vault operations and operating costs, efficiently utilizing human resources and improving the quality of treasury services.

The digitization of cash and vault operations is not merely a trend but an imperative choice within the context of digital transformation in banking operation and the economy. The outcomes of digitization and automation solutions for cash operation process implemented by commercial banks worldwide have affirmed clear benefits in terms of operational and management efficiency, risk control, cost and resource optimization, thereby contributing to enhancing the competitiveness of credit institutions, improving liquidity management efficiency in the economy, and supporting socio-economic development. However, it also includes numerous risks and challenges related to technology, operational risks, human resources, financial resources, processes, and management. These conduct evaluations, forecasts, and develop appropriate, effective cash operation digital transformation roadmaps with synchronous integration capabilities into the bank's digital ecosystem, to ensure an efficient and sustainable digitization process for the entire banking system.

2. Current status and prospects of cash operation digitization in Vietnamese Banking system

2.1. Cash Operation Digitization in Vietnamese Banks 2012–2024

a. Period of 2012–2015 (Foundational period): The period 2012–2015 marked the initial steps of the digitization process for cash and vault operations within Vietnamese commercial banks. Information technology began to be applied to modernize internal cash management procedures; however, the level of automation and modernization remained limited and unsynchronized. From a management perspective, driven by the urgent need to modernize cash and vault operations, since 2011, the State Bank of Vietnam (SBV) commenced research and development of the CMO software (Currency Management Optimization), a centralized cash management and issuance system for the SBV. CMO was one of the crucial information technology systems that enabled the SBV to optimize cash management across Vietnam which defined the SBV's position as one of the first central banks in Southeast Asia to successfully operate a technological system for cash management. In commercial banks, cash operation procedures such as periodic inventory checks and basic camera surveillance in branch vaults began to receive initial attention.

However, the operation of the SBV's centralized cash management and issuance system still faced numerous shortcomings, such as the lack of application of modern technologies, absence of real-time management, and incomplete synchronization of customer’s cash transaction with credit transaction systems. Many stages remained manual, with limited analytical and forecasting capability. For commercial banks, most of the vault and precious asset management was still performed manually or based on traditional ledgers and simple internal software; a centralized cash management system had not yet been established. Cash deposit, withdrawal, and inventory processes remained manual and cash operation data had not been synchronously integrated with core banking systems.

b. Period of 2016–2020 (enhancement and expansion): 2016–2020 period marked a significant transformation in the digital conversion process of Vietnamese commercial banks in the cash operation sector. During this time, many large banks implemented modernization projects for banknotes and vault operations, gradually reducing manual procedures, applying information technology to cash and vault operations workflows and launching digitization projects focused on developing cash management software and centralized databases. Furthermore, the model of centralized cash operation was established with some regional centralized cash management centers, progressively linking vault management across certain areas or the entire banks.

Nevertheless, by the end of this period, the proportion of paper document and record storage remained substantial; over 80% of banks had not integrated cash and vault operations procedures into their core banking systems; and only about 10% of banks possessed real-time cash inventory tracking capabilities. This indicates that the level of bank cash operation digitization was uneven and still limited in terms of comprehensive integration of cash operation into core banking, application of modern technological solutions, and centralized cash management.

c. Period of 2021–2024 (Comprehensive Digital Transformation) This period witnessed the comprehensive digital transformation within the banking sector (where many commercial banks achieved 90% of transactions through digital channels; and numerous banking operations, such as deposits, payments, card issuance, and e-wallet connectivity which mostly achieved 100% digitized transformation), the digitization of bank cash operation continued to accelerate during the 2021–2025 period. Cash operation in Vietnamese banking system underwent significant changes compared to the initial 2012–2015 period; a large proportion of cash operation process stages achieved a relatively high level of automation, making vault operations faster, more transparent, and more secure. According to reports from the SBV and commercial banks, the digitization rate of internal cash operation within commercial banks in 2021–2025 period reached approximately 80%, representing a fourfold increase in comparison with the 2012–2015 period and a 1.5-fold increase compared with the 2016–2020 period. Numerous manual tasks in cash and vault management and various stages of cash and vault operations procedures (e. g., data entry, inventory, fund replenishment planning, online cash transaction tracking, counting, automatic reconciliation) have been automated with the assistance of machine, equipment, software, and modern technologies.

However, the digitalization of cash operation remains mostly unsynchronized (primarily concentrated some state-owned commercial banks with strong financial capability); some stages of cash and vault operations procedures have not yet been digitized; cash and vault operations workflows have not been innovated, and personnel competency did not yet meet digitization requirements; the smart vault center model has not been fully developed.

2.2. Prospects for cash and vault operations digitization in banking system during 2025–2030

According to a survey by Le Ngoc Lam and the research team (April 2025) (Survey of the project research team conducted on 30 Vietnamese credit institutions, April 2025 which illustrated the level of digitalization, digital maturity and technologies applied in cash and vault operation and management and prospect for digitalizing cash and vault operation in the period 2026–2030.), the prospects for cash and vault operations digitization in the 2026–2030 period are assessed as positive, with approximately 23.3% of credit institutions forecasting strong development in cash operation digitization. In contrast, 16.7% evaluate the prospects as moderate (little change compared to the present), and 16.7% of credit institutions believe that cash and vault operations digitization will face numerous risks.

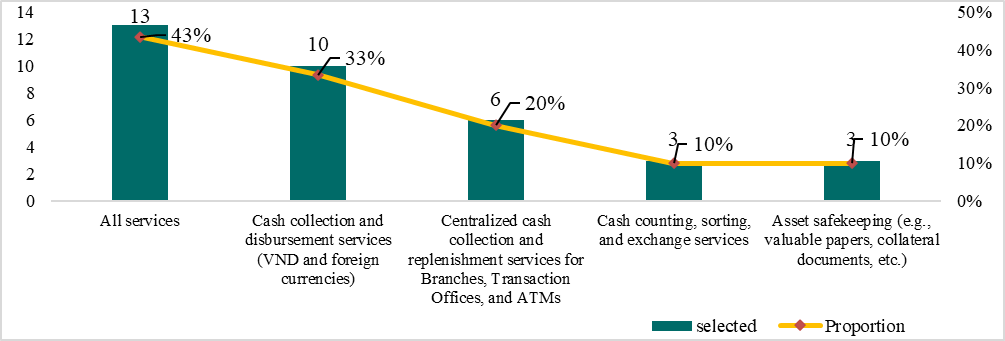

Fig. 1. Outlook banknotes and vaults operations services (Source: Le Ngoc Lam and the research team, April 2025)

In the figure 1: Survey conducted on selected 30 commercial banks in Vietnam, of which 13/30 (43%) desire a full suite of banknotes and vaults operations services, reflecting an inevitable trend of optimizing cash management, enhancing operational efficiency, and expanding customer offerings. Given core services like cash collection and payment would be crucial, the preference for integrated solutions underscore an evolution in the modern treasury landscape. This trend suggests a collective inclination among banks towards a holistic treasury solution, moving beyond a focus on fragmented, standalone services. This demand is likely driven by strategic objectives to optimize cash management operations, enhance overall operational efficiency, and cater to the diverse needs of their clients. Moreover, the survey showed the core service of cash collection and payment services (covering VND and foreign currencies) are recognized as priority or core services, accounting for approximately 33% (10/33) of service selections, being lower than the segment of banks opting for "all banknotes and vaults operation services", showing the transition from single-services to integrated service models, the progressive advancement in contemporary banknotes and vaults service trends. 20% Vietnamese commercial banks selected centralized cash collection and replenishment services for branches, transaction offices and ATMs; the remains 20% selected standalone services including cash counting, sorting and exchange services, asset safekeeping (valuable papers, collateral documents...etc.) thanks to stable internal system or their services have not yet been automated deeply to connect with high-tech services.

Regarding factors positively impacting the prospects of cash and vault operations digitization, 70% of credit institutions assess that the SBV's change in the organizational model for cash and vault operations management (the central bank's operations have been scaled down, consolidating into 15 regional branches instead of the previous 63 regions) will be a positive factor for treasury services in the next 3–5 years. The trend of shifting from self-operated cash and vault operations to outsourced cash services is expected to increase, supported by the completion of the legal framework and the facilitation and assistance from the SBV and regulatory bodies for this model, thereby helping credit institutions reduce costs and personnel for cash and vault operations. In comparison with the Technology – Organization – Environment model (TOE) (Technology – Organization – Environment (TOE) three factor model: the readiness and ability to implement technological innovation based on three factors: Technology (infrastructure, security), Organization (structure, personnel, culture, leadership commitment) and Environment (competitive pressure, regulations, market trends), the environmental factor (competitive pressure, customer expectations) strongly influences the digitization prospects of credit institutions, while organizational and technological factors play a limited role. Many banks still lack a specific roadmap, training resources, or an effective change management model, leading to confusion in the implementation of cash and vault operations digitization.

Regarding risks and challenges, credit institutions identify the main barriers to cash operation digitization in Vietnam as currently including:

- Primarily due to the impact of global economic and financial market fluctuation, changes in monetary policy management (especially with the increasing development of central bank digital currency – CBDC);

- A legal system that has not been kept pace with the speed of cash operation digitization;

- Unsynchronized information technology infrastructure of credit institutions system;

- According to the UTAUT model (Unified Theory of Acceptance and Use of Technology) (The model consists of four factors: Performance Expectancy, Effort Expectancy, Social Influence, and Facilitating Conditions), a low level of readiness among some credit institutions in the process of cash digital transformation, a reluctance to change traditional process due to weak internal communication, concerns about insufficient capital and highly skilled personnel;

- High investment costs for cash operation digitization (especially for centralized cash management systems – CMS, IOT devices, security; AI/ML technologies, etc.);

- The slow pace of customer behavior change and adoption of digital technology and process in cash operation (the preference for cash remains relatively high).

3. Technological solutions for comprehensive digitization of cash and vault operation and management in the Vietnamese commercial banking system during 2026–2030

Building upon the technology achievement applied at some leading global banks in cash operation digitization and through research, innovation, and the integration of new technologies, this study concentrates on specialized technology solutions applicable to all components of commercial bank cash and vault operations in Vietnam. The aim is to achieve comprehensive and synchronous digital transformation of Vietnamese bank cash operation during the new development phase of 2026–2030.

3.1. Technology Foundation

Fig. 2. Technological foundation for Digitizing bank cash and vault operations (Source: survey by Le Ngoc Lam and the research team, April 2025)

The figure 2, exposed the technology solutions applied in retail commercial banks in Vietnam in optimistic scenario, all steps are transformed and digitalized with technologies bellows:

- EKYC and Biometric technologies for customer/user authentication.

- Open API: Implementation of international data security standards through rigorous encryption and access management protocols, enabling mobile applications (Mobile App) to access and interact with commercial banks' internal APIs.

- Google API and optimal routing algorithm: To determine optimal routes for cash in transit, reducing transportation time and costs.

- Artificial Intelligence (AI) and Machine Learning (ML): To analyze transaction behavior, forecast cash demand by customer segment, transaction type, denomination, in real-time; accurately predict cash levels at ATMs; optimize cash replenishment schedules.

- Robotic Process Automation (RPA): To automate repetitive manual tasks such as processing warehouse entry/exit documents, accounting documents, and transaction reconciliation.

- Optical Character Recognition (OCR): To scan and extract information from receipt/payment vouchers, statements, automatically inputting data into the system.

- Enterprise Content Management (ECM): Used for digitizing documents and managing internal cash and vault operations records, converting contracts, minutes, receipts, and payment vouchers into electronic form.

- Barcode/QR code: Utilized to encode and scan information on cash bags, withdrawal/deposit slips, and seals, enhancing accuracy in management and retrieval.

- RFID (Radio Frequency Identification): Attaching tracking chips to cash bags and safes to automatically monitor cash movement within the vault, increasing the accuracy of inventory operations.

3.2. Overall Architecture of the Model

Overall, the technological solution system is built on a Micro Frontend, Micro Service architecture, enabling flexible expansion, maintenance, and integration of new digital banking services in the future. Concurrently, it ensures high performance, reliability, and security, meeting Basel II, III standards and the regulations of the SBV of Vietnam and other regulatory bodies. The effective combination of technologies assists commercial banks in operating a modern cash and vault operations management and workflow model based on a three-tier structure (policy and strategy management level; centralized oversight level; and cash operational units such as cash centers, transit points, and branches).

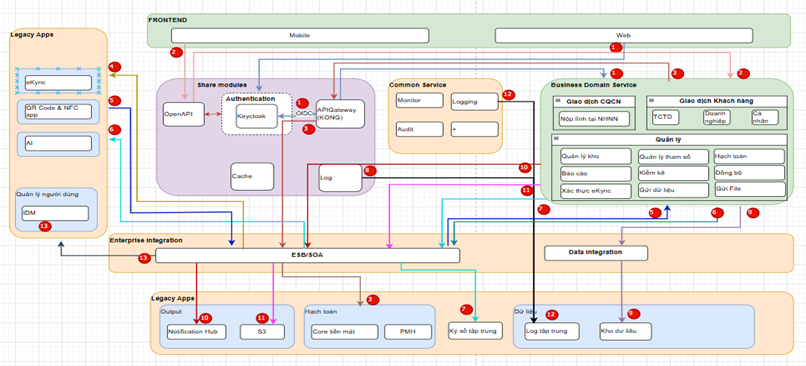

Fig. 3. Integrated architecture of the technological solution system for digitizing cash and vault operations in Vietnamese Banks during 2026–2030 Source: Le Ngoc Lam and the research team

The figure 3 above draws main components of the Technological Solution which includes crucial parts mentioned bellows:

- Component for cash operations officers (Mobile App): A mobile application developed on the Flutter SDK platform, ensuring system security through a Mobile Device Management (MDM) system. This mobile application for cash operations personnel will support operational activities such as periodic/emergency cash replenishment for ATMs, CDMs, point-of-sale (POS) terminals; inventory counting, cash inflow/outflow, and real-time cash reserve tracking.

- Counter Operations Component for Individual Customers (Micro Frontend): Replacing traditional Teller solutions, processing deposit/withdrawal transactions at customer locations, data reconciliation, securing transactions with JWT tokens, and managing access control via RBAC (Role-Based Access Control).

- Customer-facing Portal Component: A user-friendly interface, synchronized across both Web platform and Mobile App, supporting the entire operational process from registration, approval, query of treasury transactions, control and confirmation of cash delivery/receipt, data aggregation, and real-time reporting.

- Backend Services Component: This serves as the core for business processing and integration with core banking systems (integrated via SOAP/XML and API). It provides internal API endpoints using Open API (Swagger 3.0) to allow applications such as Smart Banking, Mobile Teller, or vault management systems to access cash information. Security adheres to digital banking standards (TLS 1.3, data tokenization, and access monitoring through centralized logging mechanisms like the ELK stack).

According to the research team's survey, alongside selecting appropriate technologies, Vietnamese commercial banks are focusing on combining technologies and collaborating with technology companies to develop specialized solutions that create differentiation and market leadership. Approximately 70% of Vietnamese credit institutions have either adopted or plan to deploy Open API and AI to automate internal systems and enhance customer connectivity. Around 17% of credit institutions have implemented or are implementing internal RPA to automate repetitive tasks in cash and vault operations, such as cash data reconciliation, balance updates, periodic reporting, scheduled cash transfer order coordination, and automatic ATM/CDM data updates. Simultaneously, credit institutions plan to combine RPA with AI and Open API to build a smart, seamless digital cash operation ecosystem. Approximately 30% of credit institutions have implemented or are implementing the IBM ECM system internally and plan to extend ECM adoption to partners and institutional clients. Several large commercial banks with strong financial capabilities (including BIDV) are pioneering research into the Smart Cash Service Center model, based on combining advanced technology with the increasing demand for modern cash and vault operations and services.

Compared to the 2021–2024 period, modern technological solutions for cash and vault operations digitization in the 2025–2030 period will offer numerous superior advantages: increased efficiency and accuracy in management and operations (automating 80–90% of cash and vault operations tasks, boosting labor productivity, real-time tracking of cash and asset reserves), optimized costs and resources, minimized risks, enhanced security, development of a modern banking ecosystem, improved service quality and compliance with international standards, active support for liquidity management and regulation in the economy, and meeting socio-economic development needs.

4. Recommendations

To support Vietnamese commercial banks in the comprehensive and synchronized digitization of cash and vault operations during the 2025–2030 period, the study proposes several key solutions:

- For the State Bank of Vietnam (SBV): The SBV needs to promptly complete the legal framework for bank cash and vault operations and digitization in banknotes and vault management, including legal provisions for the Smart Cash Service Center model, updating and amending regulations on the delivery, safekeeping, and transportation of cash, precious assets, and valuable papers, and accepting digital signatures. New standard regulations for vault security are also required for applied technologies such as AI camera surveillance, biometric access control, specialized vehicle GPS tracking, electronic vault doors, and electronic safe locks; data encryption, two-factor authentication, data backup, etc.; and regulations on inspection and examination. Concurrently, the SBV should focus on investing in modern technological infrastructure capable of synchronous integration with the commercial banking technological ecosystem and the future Smart Cash Service Center model. This will enhance the efficiency of cash management and coordination, create a closed-loop cash and vault operations processing environment, and improve the quality and accuracy of statistical reporting and forecasting systems.

- For Commercial Banks (CBs): Commercial banks in Vietnam need to accurately assess their current status of cash and vault operations digitization using scientific models (TOE, TAM, Digital Maturity), incorporating international best practices and insights from leading domestic banks in cash and vault operations digitization. This will enable them to develop a methodical and effective digital transformation plan, ensuring flexibility, standardization, and integration with core technological systems (core banking, TMS). Furthermore, they should select open, highly integrated technological solutions that align with the technological infrastructure trends and are suitable for the Smart Cash Service Center model – an inevitable trend in banking cash and vault operations. Alongside with the process of applying modern technologies and developing modern treasury products, commercial banks must focus on restructuring their organizational models, processes, and human resources towards a lean, efficient approach, consistent with each bank's level of cash and vault operations digitization.

- For technology, payment and cash management companies: Enhance cooperation with commercial banks in cash and vault operations digitization: Research and develop software platforms and digital applications to support cash and vault operations, ensuring these digital platforms are stable, highly secure, and compatible with the digital banking ecosystem. Focusing on researching trends and the development of the Smart Cash Service Center model will enable technology companies to achieve a pioneering position in providing technological solutions for modern Cash Service Centers within the Vietnamese commercial banking system.

In summary, the digitization of cash and vault operations in Vietnamese banks has made remarkable strides, becoming a crucial link in the comprehensive digital transformation of the banking sector. The prospects for bank cash and vault operations digitization in the 2025–2030 period are assessed relatively positive. However, numerous risks and challenges persist from the external environment, competitive pressures, and from commercial banks themselves. The acquisition of international experience to maximize benefits, mitigate risks, and positively contribute to the overall digitization process of the Vietnamese banking sector. By focusing on researching and collecting lessons from global commercial banks and establishing a clear roadmap that synchronizes technology, human resources, risk management, and performance measurement, Vietnamese commercial banks cash and vault operations in the 2025–2030 period are projected to reduce costs by 20–30%, increase productivity by 1.5–2 times, aiming to become a value-creation center, yielding increasingly high economic efficiency for banks and the economy.