.png&w=384&q=75)

1. Introduction

With the intensification of global climate change and the rising prominence of sustainability issues, Environmental, Social, and Governance (ESG) concepts have moved from peripheral discourse to the center of corporate strategy. Since China formally proposed the goals of "carbon peaking by 2030 and carbon neutrality by 2060" in 2020, the integration of ESG principles into business operations has become both a policy imperative and a market expectation. The China Securities Regulatory Commission (CSRC) and the three major stock exchanges have successively issued sustainability reporting guidelines, marking the gradual establishment of a structured ESG disclosure framework in China.

Power enterprises occupy a pivotal position in this transformation. As one of the largest sources of carbon emissions in China, the power sector is at the forefront of the energy transition. Simultaneously, power enterprises bear substantial social responsibilities including ensuring stable electricity supply and supporting rural electrification. The convergence of environmental urgency, social expectations, and governance reforms makes the power industry a critical lens through which to examine ESG-driven value creation [5, p. 3643]. This paper aims to clarify the theoretical logic and empirical pathways through which ESG concepts enhance the value of Chinese power enterprises and offer policy recommendations.

2. Theoretical Foundations and Literature Review

ESG refers to a comprehensive evaluation framework encompassing Environmental, Social, and Governance dimensions. Three theoretical perspectives underpin its relationship with corporate value. Stakeholder theory [1] posits that long-term enterprise value depends on balancing the interests of all stakeholders. Signaling theory suggests that high-quality ESG disclosure reduces information asymmetry, while the resource-based view treats ESG investments as intangible strategic resources generating sustainable competitive advantages.

Existing studies generally support a positive correlation between ESG performance and enterprise value. Friede, Busch, and Bassen (2015) aggregated approximately 2,200 individual studies and confirmed that the business case for ESG investing is empirically well founded. Wong et al. (2021) demonstrate that ESG certification reduces the cost of capital and significantly increases Tobin's Q. Within China, Wongvanichtawee (2023) shows that ESG disclosure positively affects firm value among listed energy companies. However, research focusing specifically on the power industry remains relatively limited [4, p. 2607], particularly regarding heterogeneous effects across power generation types–a gap this paper seeks to address.

3. Mechanisms of ESG Concepts in Enhancing Enterprise Value

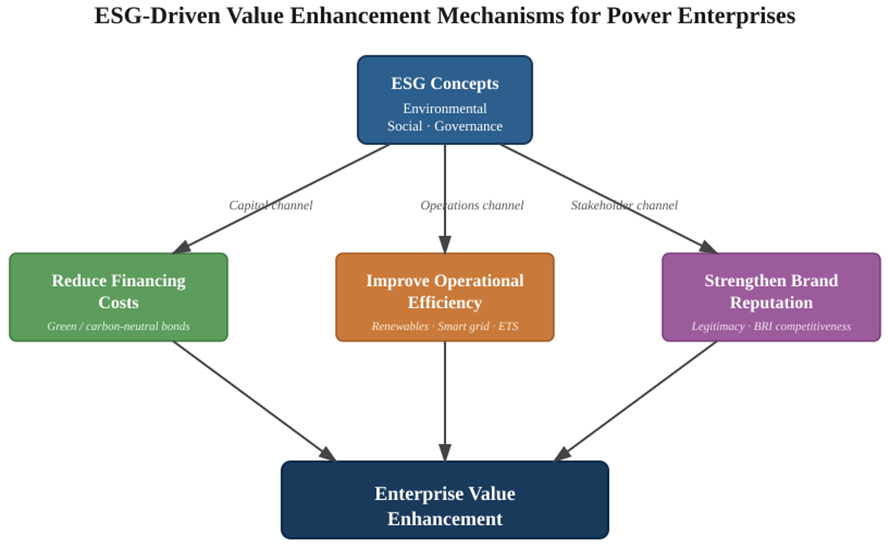

Building on the theoretical perspectives above, this paper proposes a tripartite mechanism through which ESG concepts enhance the value of Chinese power enterprises, as illustrated in Figure. Three transmission channels–the capital channel, operations channel, and stakeholder channel–jointly translate ESG performance into enterprise value enhancement.

Fig. Theoretical framework of ESG-driven value enhancement (compiled by author)

3.1. Reducing Financing Costs through Green Finance

ESG performance directly affects power enterprises' access to and cost of capital. Power enterprises with strong ESG ratings can issue green bonds, sustainability-linked bonds, and carbon-neutral bonds at favorable terms. China's first batch of carbon-neutrality-themed green bonds, issued in 2021 by six leading enterprises including China Three Gorges Corporation, China Southern Power Grid, and State Power Investment Corporation, raised 6.4 billion yuan primarily for wind, hydropower, and photovoltaic projects. Wong et al. (2021) provide empirical evidence that ESG certification significantly lowers the cost of capital and expands investment capacity for clean energy projects.

3.2. Improving Operational Efficiency through Green Transformation

Embedding ESG principles into operations drives technological innovation and efficiency improvements. Wang et al. (2024) demonstrate that for Chinese listed thermal power enterprises, environmental regulation significantly enhances green investment efficiency, with the proportion of installed renewable energy capacity steadily growing alongside ESG index improvements. Furthermore, participation in the national carbon emission trading market transforms emissions reduction from a regulatory burden into a potential revenue stream [7, p. 10478].

3.3. Strengthening Brand Reputation and Market Position

Strong ESG performance enhances corporate reputation among customers, regulators, and the public. For state-owned power enterprises, ESG leadership reinforces social legitimacy and supports their operating mandate. For private and listed power enterprises, ESG branding improves competitiveness in international tenders, particularly under the Belt and Road Initiative. Robust ESG governance also reduces litigation risks and reputational damage [8, p. 1-18]. To compare ESG practices across power generation types, Table summarizes the differences between thermal power and renewable energy enterprises across key ESG dimensions.

Table

Comparison of ESG Practices Between Thermal Power and Renewable Energy Enterprises (Compiled by author based on cited references)

Dimension | Key Indicator | Thermal Power | Renewable Energy | Reference |

Environmental | CO₂ emission intensity | High | Low | Kong et al. (2024) |

| Green investment efficiency | Improving | High | Wang et al. (2024) |

Social | Stable supply / public service | Strong | Moderate | Long & Gao (2018) |

Governance | ESG disclosure quality | Mixed | Improving | Wongvanichtawee (2023) |

Value Outcome | Cost of capital | Higher | Lower | Wong et al. (2021) |

| Tobin's Q (firm value) | Moderate | Higher | Huang et al. (2023) |

4. Current Status and Challenges

Major Chinese power enterprises have made notable progress in ESG practices, with the proportion of A-share listed power companies publishing standalone ESG reports rising substantially after the 2024 disclosure guidelines from the three Chinese stock exchanges. Leading enterprises such as China Yangtze Power are recognized for proactive sustainability practices. However, key challenges persist: ESG disclosure standards remain fragmented across GRI, SASB, TCFD, and CSRC frameworks; data quality and verification mechanisms are underdeveloped, raising concerns about "greenwashing"; thermal power enterprises face transformation pressures where short-term capital expenditures may depress earnings before benefits materialize [6, p. 8417]; and regional disparities remain significant, with eastern coastal enterprises generally outperforming central and western counterparts [7, p. 10478].

5. Recommendations and Conclusion

At the policy level, regulators should accelerate the unification of ESG disclosure standards by issuing power-industry-specific guidelines, progressively introducing mandatory third-party assurance for key indicators. Fiscal incentives such as preferential tax rates and accelerated depreciation for green technology investments would mitigate short-term cost pressures. At the enterprise level, power companies should integrate ESG into core strategic planning, establish board-level ESG committees, link executive compensation to ESG performance, and embed ESG risk assessment into investment decisions. At the capital market level, expanding green and sustainability-linked bonds [10], launching ESG-themed ETFs, and improving the credibility of domestic ESG rating agencies will channel capital toward high-performing enterprises.

In conclusion, ESG concepts represent both a challenge and an unprecedented opportunity for Chinese power enterprises. Through reducing financing costs, improving operational efficiency, and strengthening brand reputation, ESG practices substantially enhance enterprise value while contributing to the national "dual carbon" goals. Power enterprises that proactively embrace ESG principles will secure long-term competitive advantages and play a pivotal role in shaping a sustainable energy future. Future research should further explore the heterogeneous effects of ESG across different power generation types using more granular firm-level data.