Disclosure statement

No potential conflict of interest was reported by the authors.

Introduction

In modern conditions, when digital technologies affect all aspects of financial services, and digital platforms become a crucial mechanism for interacting with existing and potential customers, institutions need to use these technologies and use changes to develop and strengthen a customer-oriented approach. Financial institutions have been focused on digital transformation since the inception of fintech, but they still have a long way to go before they become truly digital. In fact, these institutions must face growing competition from fintech startups and technology giants, which are already exerting competitive pressure on the banking sector through constant innovation. In fact, this is already an "interspecific competition", where banks must use the full range of their competitive advantages to maintain their dominant positions in the financial services market.

The introduction of digital technologies can increase the trust and interest of customers, which will allow banks to better understand their customers and develop services that best suit them. They also can reduce operating costs while complying with increasingly complex and constantly changing regulatory requirements and at the same time market demands. In a financial institution, digital transformation occurs because of a fundamental reform of internal and business processes. But, most importantly, it leads to a change of thinking in the methodology of the banking sector. It is safe to say that the true meaning of changes in the direction of digitalization of the banking business lies in the modern way of creating value and increasing income. As a result, already at the present stage, some banks have optimized the branch network [1].

The Ministry of Finance of Ecuador is responsible for the development and implementation of fiscal policies that guarantee the sustainability, stability, and transparency of public finances. The banking system of Ecuador is two–tier, the regulator of the banking market is the Central Bank of Ecuador (CBE), which was conceived as a reserve bank when the system of dollarization of the Ecuadorian economy was initially introduced. The main difference in the characteristics of the digital transformation of the Russian and Ecuadorian banking sectors is that the digital currency in Ecuador has already been launched and tested. Moreover, “Dinero Electrónico” is not only tested and used, although not as widely as it could be. In Russia, the digital ruble as of the beginning of 2022 is in the process of testing. But after its introduction, the use of the Russian digital currency is likely to be more systematic and widespread.

The Russian and Ecuadorian banking sectors have much more similarities:

- Platformization, diversification and customer orientation based on AI.

- The ubiquity of mobile payments (but here, at the moment, Ecuador has an advantage in terms of using digital currency).

- Optimization of banking business processes to increase their automation and security.

Nevertheless, it should be noted the general problem of the digital development of the Ecuadorian banking system in terms of digital transformation. In general, Ecuador's digital transformation process, having passed the initial period, is currently stagnating. This is due to the general systemic weakness of the public administration system, which does not create a strong incentive base for further digital transformation of the economy.

Assessment of the state and speed of development of digital economies

In Russia, the digital transformation of the economy is taking place at a significant pace: Russia is promising in this regard, although it does not belong to the world leaders of digital transformation, with the pace of digital development above average [2]. At the same time, Ecuador belongs to the countries with a lower-than-average rate of digital development that are problematic in terms of their digital development. Therefore, if we consider the prospects for the functioning of the digital currency, a more optimistic prospect is seen for the ruble, since it will be introduced systematically and function in a state of continuous improvement of its support system.

For Ecuador, Russia's experience is important precisely in terms of digitalization of the banking sector, because, despite an earlier start with digital currency, the lag in the direction of systemic digitalization does not allow either to fully use the advantages of using digital currency, nor to develop the banking system in general in accordance with the requirements of the modern economy.

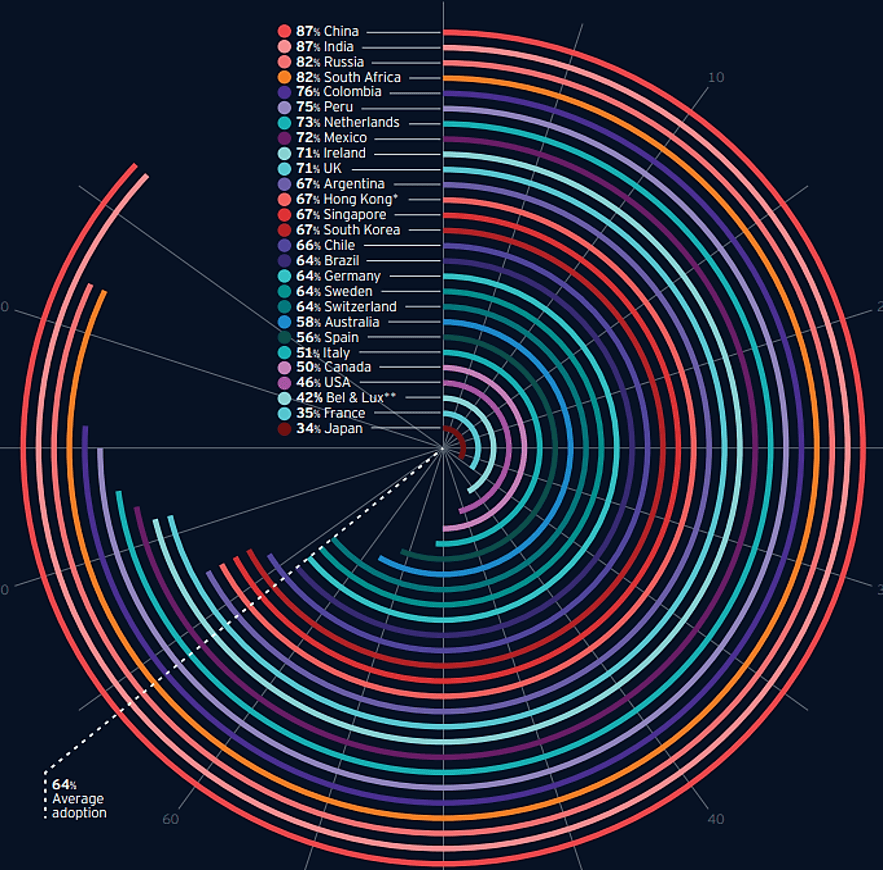

The digitalization of the economy in Russia is systemic. This means that the introduction of the digital currency (ruble) was preceded by a long period of creating a solid fundamental base. Russia today is at the forefront of digitalization of the banking sector. According to the rating of the introduction of FinTech consumer technologies in the most "advanced" markets, Russia is in 3rd place after the undisputed leaders of the introduction of China and India (Russia has an implementation rate of 82%, that is, 82% of banking users are involved in the use of digital technologies). For comparison, in Ecuador, this figure is 21%) [3].

In Russia, the neobanking segment is formed in conditions of fierce competition with the largest banks – Sberbank, Gazprombank, VTB, Otkritie Bank and others. Existing and new neobanks operate according to one of five models: independent startups operating under the license of a partner bank (Talkbank), digital banks with their own license (Tinkoff, Modulbank and Bank 131), services operating under their limited licenses (HUMOPEU), banks using the license of a credit institution of which they are a branch (Delobank, Dot) and fintech products of the company (digital bank is a product of a company or a corporate startup - Megafon Bank, Sphere, Just Bank, Elba Bank) [4]. Neobanks are most often focused on a narrow niche of customers – gamers, wealthy clients or individual entrepreneurs in the service sector with a need for premium cards. Additional niche services give such fintech services another source of income.

Fig. 1. Introduction of FinTech consumer technologies in 27 markets

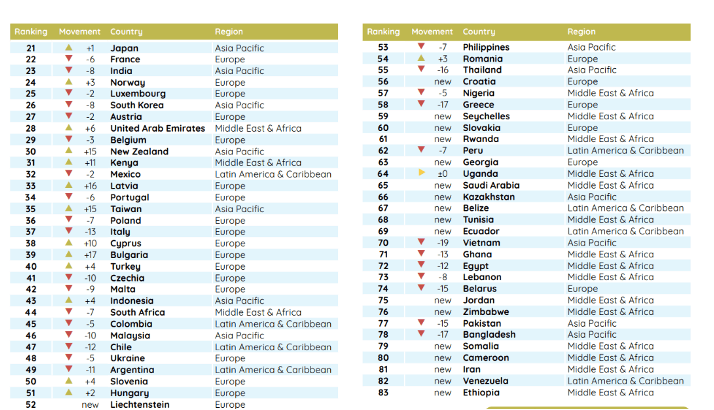

The Global Financial Technology Ranking of 2021, prepared by Mambu, identifies new centers, fintech companies and trends. The Index algorithm ranks fintech ecosystems of more than 230 cities in 65 countries, including data from findexable's own records, as well as data collated and verified by its Global Partner Network, including Crunchbase, StartupBlink, SEMrush and more than 60 fintech associations around the world. The index was first published in 2019 and has become very widespread in the financial technology industry.

The rating of a country and a city is calculated on the basis of a total score consisting of a combination of three indicators:

- Number – Size of the fintech ecosystem and supporting structures – number of fintech companies, fintech hubs, coworking, accelerators, global influencers and the population (countries only).

- Quality – Impact/performance – size and growth of fintech companies (e.g. number of unicorns), investments, events, value creation, international cooperation, website ranking.

- Environment – ease of doing business, critical mass, regulatory environment - regulatory interventions to improve the competitive environment, incentives for startups, Internet censorship, payment portals, financial technology courses.

Fig. 2. Fintech Country Rankings 21-83

It should be noted that the reason for the "failure" in the financial market of Ecuador's digital currency lies precisely in the insufficient level of digitalization of the economy as a whole and at the same time the low level of introduction of financial technologies in the banking sector. Therefore, there is no basis on which such a serious technological tool as a digital currency is "built".

The COVID-19 pandemic has had a serious impact on the global economy and the banking sector, giving fintech an uncontested priority in shaping the competitiveness of modern banks. Russian banks, being at the forefront in terms of digitalization, turned out to be more prepared for the consequences of quarantine restrictions than many foreign banks [7]. Accelerating digital transformation is one of the main tasks today to preserve the stability of the banking sector. A well-developed digitalization strategy is necessary to reduce risks, modernize compliance and develop an integrated management system.

Banks have no other strategic alternative than to face the challenges of digital structural changes and to revise their operating models. By strategically linking their business to the vast amount of data available to them, they can get information about dynamically changing customer needs, which can add value. Nevertheless, to remain competitive in the "buyer's market", banks must accelerate the digitization of business. Customers want accounts to be opened in minutes and expect banks to have access to all their data. Round-the-clock availability, intuitive interfaces, real-time execution, and an individual approach with global consistency and error-free become the determining factors, while the main products and services turn into a commodity [8].

In addition to automating existing processes, banks should reduce complexity and response time in all interactions with customers, as well as develop automated decision-making, more effectively complying with regulatory requirements. Data management and analytics platforms are crucial for this. They provide customer insight, faster and more efficient decision-making, and reliable performance tracking. New specialists may be needed inside banks, for example, data processing and user interface designers [9]. Nevertheless, credit institutions should focus on their core strengths and, if necessary, seek internal and external strategic partnerships to expand their capabilities. They also need to maintain momentum: track progress towards achieving their goals with appropriate KPIs and tell success stories that help change the culture of the organization. Equally important is the need to encourage employees at all levels to identify new practices and opportunities that will contribute to further development and achieve high results.

The prospects for the digital development of the banking business are promising. Integrated digital banking will become even more connected to everyday life when everyday household items are connected to the Internet, and the right to consumer data will apply to all sectors of the economy (apart from OpenBanking). Its importance will increase exponentially as disparate data sets merge to provide a 360-degree comprehensive picture of our lives [10].

Conclusion

That the further in Ecuador, the most urgent problem of the introduction and dissemination of digital technologies in the banking sector is its unavailability. For Ecuador, the experience of Russia as one of the world leaders of fintech in the banking industry would be very relevant. Digitalization of banking services, the introduction of digital tools for end users, will certainly allow to "revive" the digital currency project of Ecuador and will make it possible to use it fully for the development of the country's financial system. First, the digitalization of the Ecuadorian banking sector will significantly reduce the cost and at the same time increase the security of banking operations (transactions, as well as supporting business processes). This will lead Ecuador to a higher position in the digital competitiveness of the banking sector.