Introduction

The integration of Environmental, Social, and Governance (ESG) factors into corporate strategies has transitioned from a voluntary initiative to an essential component of modern business practices. ESG risks – encompassing environmental challenges, social responsibilities, and governance inefficiencies – are increasingly recognized as critical determinants of corporate performance and long-term sustainability. These risks not only affect operational resilience but also directly influence profitability, financial stability, and stakeholder confidence [8, p. 210-233]. Companies worldwide are adapting their strategies to address these risks, embedding ESG considerations into their operations and disclosures to align with evolving stakeholder expectations.

Global regulatory frameworks reflect the growing importance of ESG practices. Initiatives such as the U.S. Securities and Exchange Commission’s (SEC) proposed rules on climate-related disclosures and the European Union’s Corporate Sustainability Reporting Directive (CSRD) mandate greater transparency and standardization in ESG reporting. These regulations are driving companies to integrate ESG factors into their Enterprise Risk Management (ERM) frameworks, ensuring that sustainability-related risks are systematically identified, assessed, and mitigated [4, p. 1056-1070]. By embedding ESG into ERM, organizations not only meet compliance requirements but also strengthen their ability to manage emerging risks and seize sustainability-related opportunities.

Stakeholders – including investors, consumers, and policymakers – are increasingly prioritizing ESG performance as a measure of corporate accountability and sustainability. Research demonstrates that strong ESG performance correlates with enhanced corporate reputation, increased investor trust, and improved financial metrics such as Return on Assets (ROA) and Return on Equity (ROE) [8, p. 210-233]. Companies that effectively integrate ESG considerations often gain a competitive advantage by fostering innovation, operational efficiency, and resilience in the face of evolving market and regulatory conditions.

At the same time, challenges persist in the effective implementation of ESG practices. These include resource constraints, the complexities of measuring and disclosing ESG impacts, and the varying expectations of stakeholders across industries and regions. Companies integrating ESG practices often need to allocate significant resources to these initiatives, particularly in emerging markets. These efforts include enhancing reporting systems, training staff, and adapting business processes to meet evolving global standards. While such investments aim to foster transparency and sustainability, the financial outcomes of ESG initiatives may not always be immediately evident. This uncertainty can pose challenges for organizations striving to balance resource allocation with profitability goals. Understanding how ESG disclosures influence financial performance is therefore crucial, especially for companies seeking to align sustainability initiatives with long-term economic viability.

Kazakhstan provides a unique perspective on the intersection of ESG disclosure and financial performance. As an emerging market with a resource-driven economy, its corporate landscape is dominated by industries such as mining and energy, which have significant environmental footprints. ESG practices – particularly environmental considerations – are therefore integral to corporate strategies, aligning with global sustainability standards and supporting efforts to enhance competitiveness in international markets.

This study examines the relationship between ESG disclosure and financial performance in publicly listed companies in Kazakhstan. By utilizing ESG scores as proxies for disclosure quality, the research evaluates their impact on key financial performance indicators, including ROA, ROE, and Return on Capital (ROC). Additionally, the study explores how sectoral characteristics, such as the prominence of resource-intensive industries, shape the relationship between ESG practices and financial outcomes.

This research contributes to a broader understanding of ESG integration in emerging markets. The findings offer valuable insights for policymakers, corporate leaders, and investors seeking to align sustainability initiatives with financial performance objectives. As ESG practices become increasingly embedded in global corporate strategies, this study highlights the potential for aligning ESG considerations with risk management frameworks to enhance both sustainability and profitability.

Literature Review

The Global Risks Report (2022) underscores the growing prominence of ESG risks compared to traditional economic risks. ESG risk, encompassing environmental, social, and governance factors, poses significant challenges for businesses across sectors. Regulatory and market pressures compel financial institutions and corporations to integrate ESG considerations into their decision-making processes [5, p. 589-605]. Such integration is essential not only for managing risks but also for enhancing corporate reputation and ensuring long-term financial stability [5, p. 589-605]. The consequences of ESG risk vary depending on the industry and activity specifics. Industries such as mining, fuel, and chemical sectors face significant environmental risks, while the hospitality and tourism industries are more exposed to social risks due to their dependence on human interaction. Moreover, digitalization and cybersecurity present governance challenges in sectors reliant on electronic service delivery [10].

Numerous studies have demonstrated the positive impact of ESG integration on financial performance. For instance, higher ESG scores are associated with improved operational efficiency, employee productivity, and corporate competitiveness [11]. Financial metrics such as ROA, ROE, and Tobin’s Q also exhibit significant improvement with better ESG performance (Cornett et al., 2016; Peng & Isa, 2020). However, some studies report mixed findings, suggesting that ESG investments may incur costs that offset potential financial gains (Duque-Grisales & Aguilera-Caracuel, 2019).

Adjustment measures towards sustainability often exceed businesses' financial capabilities, necessitating external financing. Financial markets conditionally provide this financing based on ESG compliance, influencing companies' ability to transform their business models (Urban & Wójcik, 2019).

The integration of ESG factors into ERM frameworks is no longer optional but a necessity for organizations (COSO & WBCSD, 2018). ERM processes now incorporate ESG risks to ensure comprehensive risk assessment and mitigation. However, existing frameworks often fall short of effectively addressing ESG risks. Challenges include the inability to quantify ESG risks monetarily, inadequate cultural integration of ERM practices across organizations, and siloed responsibility for ESG concerns within sustainability divisions (World Business Council for Sustainable Development, 2017).

Despite these challenges, the alignment of ERM with ESG initiatives enhances stakeholder confidence and corporate value. Studies highlight the moderating role of ESG performance in strengthening the relationship between ERM and financial outcomes. For instance, Shad et al. (2019) proposed a conceptual model linking ERM, ESG, and firm performance, emphasizing the need for empirical validation of this framework.

The role of financial markets in facilitating ESG integration is well-documented. Financial institutions incorporate ESG factors into lending and investment decisions, often influencing the cost of capital. For instance, companies with higher ESG scores enjoy lower borrowing costs and higher credit ratings (Henriksson et al., 2018). Conversely, poor ESG performance correlates with higher credit risk and financing costs (Eliwa et al., 2019).

Empirical studies have shown that ESG disclosures significantly influence capital allocation decisions. The ASEAN-Japan Center (2019) revealed the global attention garnered by investments incorporating ESG factors, particularly in Asia. However, records indicate that existing risk management practices are insufficient in addressing ESG-related risks (World Business Council for Sustainable Development, 2017).

The transition to sustainable business models is a critical aspect of ESG integration. Such transformations often require external financing, given the substantial costs involved. Financial institutions act as intermediaries, supporting enterprises in their sustainability endeavors [14, p. 1-19]. The alignment of corporate strategies with ESG principles not only enhances financial performance but also contributes to societal well-being (Godfrey, 2010).

Despite the importance of ESG integration, the World Business Council for Sustainable Development (2017) highlighted three primary challenges. Firstly, ESG risks are difficult to quantify in monetary terms, complicating resource allocation. Secondly, ERM must be embedded as a cultural norm across all organizational levels. Lastly, ESG risks are often seen as the sole responsibility of sustainability divisions, leading to imbalanced risk management approaches.

Despite the growing body of literature on ESG, limited research explores its specific impact within emerging markets such as Kazakhstan. Furthermore, the role of financial system models in shaping ESG disclosure and performance remains underexplored. This study addresses these gaps by focusing on the Kazakhstani context, providing empirical evidence on the relationship between ESG disclosure and financial outcomes. To ensure robustness, the regression analysis employed ESG scores and their components (E-score, S-score, and G-score) as independent variables. Control variables included firm size, asset turnover ratio, leverage ratio, and asset growth. These variables, ranging from 0 to 100, were evaluated using a pooled panel data model to establish the influence of ESG factors on financial performance.

Methodology

This study examines the relationship between ESG (Environmental, Social, and Governance) indicators and the financial performance of public companies in Kazakhstan. The research covers 50 publicly listed Kazakhstani companies over the period from 2010 to 2019, resulting in a total of 361 observations. Companies were included in the sample if they provided information on all four ESG factors (detailed later) for at least one year within the study period. All companies in the sample disclosed some degree of ESG information.

The selected companies represented nine industries based on international classification standards. However, the industry comparison focused on two sectors with the highest number of observations: materials (129 observations) and utilities (88 observations). The materials sector comprised companies involved in metals and ores, construction and chemical products, containers and packaging, and pulp and forest products. The utilities sector included companies offering electric, gas, multi-utility, and water supply services. Companies from other industries were excluded from comparative analyses due to insufficient representation.

The research employed traditional financial analysis, utilizing accounting-based profitability metrics, including return on assets (ROA), return on equity (ROE), and return on capital (ROC). These indicators are widely used by creditors and investors due to their reliance on verifiable data from audited financial statements [Luo, 2015; Aras et al., 2010]. The quality and extent of ESG disclosure were evaluated using the ESG score, calculated from Bloomberg database data. Financial information was also sourced from the same database. Industry classification adhered to the Bloomberg Industry Classification Standard (BICS).

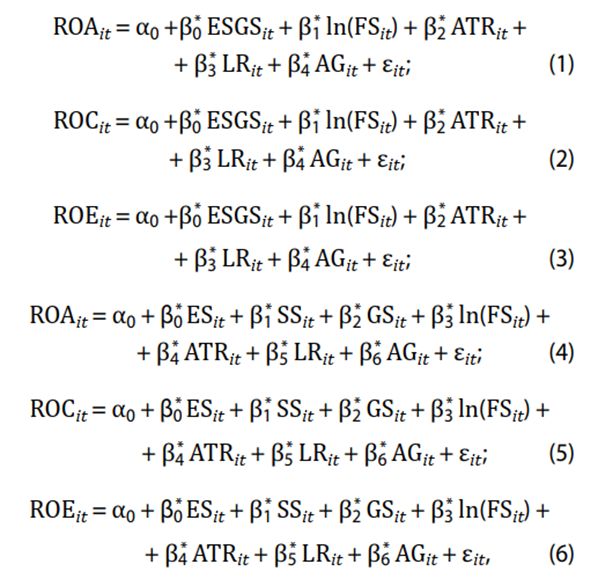

A regression analysis was conducted to examine the influence of ESG factors on financial performance. Independent variables included the overall ESG disclosure score (ESG-score, ESGS), as well as the scores for environmental (E-score, ES), social (S-score, SS), and governance (G-score, GS) factors. These scores range from 0 to 100. Control variables included firm size (natural logarithm of total assets, ln(FS)), asset turnover ratio (ATR), leverage ratio (LR), and asset growth (AG). A pooled panel data model was used to estimate coefficients for independent and control variables.

Table 1

Variables and their definitions

Variable | Definition |

| Coefficients estimating the impact of ESG factors on financial performance (corresponding variables are marked with an asterisk) |

| Return on assets |

| Return on capital |

| Return on equity |

| Overall ESG disclosure score |

| Environmental disclosure score |

| Social disclosure score |

| Governance disclosure score |

| Natural logarithm of the company’s total assets |

| Asset turnover ratio |

| Leverage ratio |

| Asset growth rate |

| Random error term |

Six regression equations were constructed, with two equations for each financial performance metric. The first equation in each pair included the overall ESG disclosure score, while the second incorporated the three individual ESG components (E-score, S-score, and G-score). The regression equations used in this study are provided in figure. Table 1 provides an overview of the variables used in the regression analysis, along with their definitions and metrics."

Fig. Regression equations

To further explore the relationship between ESG disclosure and financial performance, the study formulates the following hypotheses:

1. There is a positive association between the level of ESG disclosure and the profitability of Kazakhstani companies.

2. The relationship between overall ESG disclosure and profitability metrics is shaped by specific company characteristics:

2.1. Extent of ESG Disclosure: It is hypothesized that companies with higher average ESG scores experience a stronger positive impact on profitability. This is because ESG disclosure tends to hold more value for investors and creditors when the ESG score surpasses a certain threshold, signaling meaningful and credible engagement with sustainability practices.

2.2. Company Size: The effect of ESG disclosure on profitability is expected to be more pronounced for smaller firms compared to large-cap public companies in Kazakhstan. Larger companies are typically subject to greater stakeholder expectations regarding sustainability initiatives due to their significant societal and environmental impact. In contrast, smaller firms, with comparatively limited potential external impact, may benefit disproportionately from ESG-related improvements in stakeholder perceptions.

2.3. Financial Leverage: Companies with higher levels of financial leverage are anticipated to show a stronger correlation between ESG disclosure and profitability. This stems from the increased demand by investors, creditors, and other stakeholders for comprehensive disclosure from firms with higher financial risk.

2.4. Industry Sector: The influence of ESG disclosure is expected to vary across industries. In particular, companies in the materials sector – such as those involved in metallurgy, mining, and other resource-intensive activities – are hypothesized to exhibit a stronger relationship between ESG disclosure and profitability. This is due to the significant environmental impact of these industries, including emissions and resource depletion, which heightens the relevance of ESG practices. By comparison, the utilities sector, while still important, may exhibit a relatively weaker association between ESG disclosure and financial performance.

Research Results

The descriptive analysis revealed an increase in observations over the study period, rising from 24 in 2010 to 43 in 2019. This growth reflects the increasing number of companies publishing sustainability reports in accordance with the Global Reporting Initiative (GRI) guidelines. Table 1 presents the descriptive statistics of the variables used in this study. The average profitability ratios for the sample were as follows: ROA – 6.72%, ROC – 10.09%, and ROE – 15.94%, while the median values were: ROA – 5.9%, ROC – 10.14%, and ROE – 14.4%. Over the study period, the disclosure of ESG information by Kazakhstani public companies increased significantly.

The average ESG disclosure score (ESGS) was 38.41, ranging from a minimum of 11.57 to a maximum of 74.51. Environmental disclosures (E-score) averaged 30.23 (median: 28.68), social disclosures (S-score) averaged 37.09 (median: 36.67), and governance disclosures (G-score) averaged 55.24 (median: 57.14). Environmental disclosures were the least developed, while governance disclosures were the most comprehensive. For instance, one company achieved a governance disclosure score exceeding 90, with an overall ESG disclosure score above 55. This highlights its inclusion in multiple international ESG ratings and recognition in global ESG rankings.

The correlation analysis demonstrated a positive relationship between profitability metrics and ESG disclosure scores across all pairings of variables. However, this influence was not statistically significant in some cases. Only ROE showed a statistically significant positive correlation with all ESG disclosure metrics, while ROA was significantly positively associated with ESGS and E-scores, and ROC with E-scores alone. These findings suggest that ESG disclosure generally exerts a positive influence on the profitability of Kazakhstani companies.

Regression analysis was performed to establish causal relationships and refine the findings. Table 2 presents the coefficient estimates for six equations. Columns 1–3 correspond to equations with the overall ESG disclosure score, while columns 4–6 include the individual components (E, S, and G scores). The results indicate that the overall ESGS score is positively and significantly associated with all three-profitability metrics (ROA, ROC, and ROE), with the strongest effect observed for ROE. The size of the company did not have a statistically significant influence on profitability metrics in this model. Notably, the overall ESGS score and its environmental component (E-score) had a statistically significant positive effect on the profitability of Kazakhstani public companies, while the social (S-score) and governance (G-score) components had negligible effects.

To further investigate Hypothesis 2, companies were grouped based on their average ESG disclosure score (criterion 1), company size (criterion 2), financial leverage (criterion 3), and industry (criterion 4):

Criterion 1: ESG Disclosure Levels

Companies with high ESGS scores exhibited significantly higher ROA values. However, no statistically significant differences were observed in ROC or ROE between high and low ESGS groups. Importantly, high ESGS scores, particularly the environmental component, significantly positively influenced profitability metrics for companies with strong ESG disclosures.

Criterion 2: Company Size

ESG disclosure had a 1.5–2 times stronger effect on profitability metrics for smaller companies compared to larger ones. In the sample, the median company size was in the mid-range of total assets, with the smallest companies having considerably lower total assets compared to the largest firms.

Criterion 3: Financial Leverage

Companies with higher financial leverage experienced a stronger relationship between ESG disclosure and profitability. The extent of ESG disclosure increased with leverage, particularly in governance-related disclosures (G-score), whereas environmental (E-score) and social (S-score) disclosures showed no statistically significant impact.

Criterion 4: Industry

ESG disclosure levels were higher in the materials sector than in the utilities sector. This is attributed to the materials sector’s significant environmental footprint, including emissions and resource extraction activities. ESG disclosure had a positive and significant impact on all profitability metrics for companies in the materials sector. In contrast, utility companies had lower overall ESGS and governance disclosure scores, with no significant relationship between ESG disclosure and profitability metrics.

Descriptive Analysis

The descriptive analysis revealed that the number of observations increased from 24 in 2010 to 43 in 2019. This increase corresponds to the growing number of companies publishing sustainability reports in line with the Global Reporting Initiative (GRI) guidelines. The descriptive statistics of the variables used in this study are summarized in table 2.

Table 2

Descriptive statistics, 2010–2019

Variable | Mean | SD | Q (25%) | Median | Q (75%) | Min | Max |

ROA, % | 6.85 | 9.1 | 2.3 | 6 | 11.1 | –42.5 | 53.5 |

ROC, % | 10.15 | 11.85 | 5.6 | 10.2 | 22.7 | –59.5 | 61.3 |

ROE, % | 16.02 | 29.2 | 4.7 | 14.5 | 15.2 | –141 | 190.7 |

ESGS | 38.5 | 13.3 | 29.4 | 37.8 | 48.4 | 11.6 | 74.6 |

ES | 30.3 | 15.8 | 18.8 | 28.7 | 41.1 | 1.6 | 79.8 |

SS | 37.15 | 16.2 | 25 | 36.7 | 49.2 | 3.5 | 75.2 |

GS | 55.3 | 14.4 | 46.5 | 57.2 | 62.6 | 18 | 94 |

FS, billion tg | 2250 | 4935 | 220 | 520 | 1165 | 42 | 31195 |

ATR | 0.65 | 0.4 | 0.43 | 0.58 | 0.8 | 0.1 | 2.65 |

LR | 3.35 | 3.7 | 1.55 | 2 | 3.4 | 1.1 | 40.1 |

AG, % | 10.7 | 32.2 | –0.15 | 7.4 | 15.2 | –52 | 417.1 |

According to table 2, the average profitability ratios for the sample were as follows: ROA – 6.85%, ROC – 10.15%, and ROE – 16.02%, with median values of ROA – 6.0%, ROC – 10.2%, and ROE – 14.5%. Over the analyzed period, ESG disclosure by public companies increased substantially. The average overall ESG disclosure score (ESGS) was 38.50, ranging from a minimum of 11.6 to a maximum of 74.6. The environmental component (ES) had an average score of 30.30 (median: 28.7), the social component (SS) averaged 37.15 (median: 36.7), and the governance component (GS) averaged 55.30 (median: 57.2). Governance indicators demonstrated the highest levels of disclosure, while environmental indicators were the least disclosed.

The correlation analysis (table 3) identified positive relationships between profitability metrics and ESG disclosure scores across all pairs of variables. However, this influence was not statistically significant in all cases. ROE exhibited a statistically significant positive correlation with all ESG disclosure scores. ROA showed significant positive correlations with ESGS and ES, while ROC was significantly correlated only with ES. These results indicate that ESG disclosure generally has a positive influence on profitability.

Table 3

Characteristics of the Sample

Industry (International Classification) | Number and Share of Observations, units/% | Number and Share of Companies, units/% |

Materials | 127/35% | 15/30% |

Utilities | 90/25% | 12/24% |

Energy | 58/16% | 7/14% |

Communications | 25/7% | 4/8% |

Financials | 21/6% | 3/6% |

Industrials | 14/4% | 3/6% |

Real estate | 12/3% | 2/4% |

Consumer staples | 11/3%s | 3/6% |

Consumer discretionary | 3/1% | 1/2% |

Total | 361/100% | 50/100% |

Regression analysis was conducted to further explore the causal relationships between the variables. The results are presented in Table 4, which provides coefficient estimates for six equations. Columns 1–3 represent models with the overall ESG disclosure score, while columns 4–6 focus on the individual ESG components (ES, SS, and GS).

Table 4

Pooled panel data regression

Variable | ROA (1) | ROC (2) | ROE (3) | ROA (4) | ROC (5) | ROE (6) |

Intercept | –1.5 | –1.8 | –7.8 | 0.6 | –0.85 | –5.5 |

ESGS | 0.1 | 0.08 | 0.4 | 0 | 0 | 0 |

ES | 0 | 0 | 0 | 0.16 | 0.12 | 0.4 |

SS | 0 | 0 | 0 | –0.06 | –0.05 | –0.08 |

GS | 0 | 0 | 0 | –0.02 | 0.01 | 0.1 |

ln (FS) | 0.3 | 0.45 | –1.3 | 0.2 | 0.4 | –1.5 |

ATR | 4.7 | 8.6 | 11.1 | 5.1 | 8.8 | 11.8 |

LR | –0.35 | –0.2 | 2.1 | –0.28 | –0.15 | 2.2 |

AG | 0.07 | 0.09 | 0.18 | 0.06 | 0.08 | 0.17 |

R2 | 0.16 | 0.16 | 0.15 | 0.18 | 0.16 | 0.15 |

Adjusted R2 | 0.15 | 0.15 | 0.14 | 0.16 | 0.15 | 0.13 |

F-statistic | 12.6 | 12.4 | 11.2 | 10.4 | 9.1 | 8.5 |

Observations | 361 | 361 | 361 | 361 | 361 | 361 |

The findings in table 3 reveal that the overall ESG disclosure score (ESGS) is positively and statistically significantly associated with all three-profitability metrics (ROA, ROC, and ROE). Among these, the strongest influence was observed on ROE. The size of the company did not show a statistically significant effect on profitability metrics in this model. Importantly, the environmental component (ES) had a statistically significant positive effect on all profitability metrics, while the social (SS) and governance (GS) components showed weak or negligible impacts.

To deepen the analysis, companies were grouped based on four characteristics: ESG disclosure levels (criterion 1), company size (criterion 2), financial leverage (criterion 3), and industry affiliation (criterion 4). The results for each criterion are as follows:

Criterion 1: ESG Disclosure Levels

Companies with higher ESG disclosure scores exhibited significantly higher ROA values. However, no significant differences were observed for ROC or ROE. Notably, the environmental component (ES) had a statistically significant positive impact on profitability metrics for companies with high ESG disclosure levels.

Criterion 2: Company Size

ESG disclosure influenced the profitability of smaller companies approximately 1.5–2 times more strongly than larger companies. In the sample, the median total assets value was around 520 billion rubles. The smallest companies reported total assets of 42 billion rubles, while the largest companies had total assets exceeding 31 trillion rubles.

Criterion 3: Financial Leverage

ESG disclosure had a stronger effect on profitability for companies with higher financial leverage. Firms with higher debt levels also tended to have higher ESG disclosure scores, particularly in the governance component (GS). However, the environmental (ES) and social (SS) components did not exhibit statistically significant effects for highly leveraged firms.

Criterion 4: Industry Affiliation

ESG disclosure scores were higher in the materials sector compared to the utilities sector, reflecting the greater environmental impact of resource extraction and processing industries. ESG disclosure positively and significantly influenced profitability metrics for companies in the materials sector. In contrast, utility companies exhibited lower overall ESG disclosure scores and weaker governance scores, with no significant relationship between ESG disclosure and profitability metrics.

These findings underscore the critical role of ESG disclosure, particularly its environmental component, in enhancing financial performance. The materials sector, due to its significant environmental footprint, shows the strongest correlation between ESG practices and profitability. Meanwhile, smaller firms and companies with higher financial leverage benefit more from targeted ESG strategies, highlighting the competitive advantage ESG practices can provide in specific contexts.

Discussion of Results

The findings of the study reveal that Kazakhstani companies are increasingly adopting ESG disclosure practices, although environmental aspects remain the least reported. Over the analyzed period, the overall ESG disclosure score increased significantly, rising from 30.73 to 47.01 points. This upward trend reflects a growing commitment to corporate transparency and sustainability, driven by increasing stakeholder expectations and alignment with global standards.

The primary hypothesis – that ESG disclosure positively correlates with financial performance–was supported, along with additional hypotheses exploring variations in this relationship by disclosure level, industry, company size, and financial leverage.

Hypothesis 2.1 which explored the differential impact of ESG disclosure on companies with varying disclosure levels, found that firms with higher overall ESG disclosure scores and strong environmental reporting exhibited statistically significant positive effects on profitability metrics. These results highlight the financial value of robust ESG reporting, particularly for firms committed to sustainability.

As outlined in hypothesis 2.2, company size influences the relationship between ESG disclosure and financial performance. Smaller companies demonstrated a stronger correlation, with ESG practices having 1.5–2 times the impact on profitability compared to larger firms. For smaller organizations, ESG reporting serves as a competitive advantage, enabling differentiation and increased investor interest. In contrast, for larger companies, ESG disclosure is often seen as a routine part of operations.

Hypothesis 2.3 was also confirmed, demonstrating that ESG disclosure has a greater positive impact on companies with higher financial leverage. These companies are typically subject to more rigorous scrutiny by creditors, who demand comprehensive ESG disclosures to mitigate perceived risks. The governance and environmental components were particularly influential, highlighting their importance in managing risk perceptions and securing financing.

The analysis further validated hypothesis 2.4, showing that the relationship between ESG disclosure and profitability varies by industry. Companies in the materials sector, which have significant environmental footprints, exhibited positive relationships between all ESG components and profitability metrics. In contrast, companies in the utilities sector showed weaker ESG disclosure scores, particularly in governance, and inconsistent links between ESG disclosure and financial performance.

Conclusion

While this study provides valuable insights into the relationship between ESG disclosure and financial performance, it also highlights several limitations. The relatively small sample size (50 companies) and the 10-year analysis period capture only the early stages of ESG reporting in Kazakhstan. Moreover, the reliance on accounting-based metrics and book values, rather than market capitalization, limits the study’s applicability to investor-focused analyses. Sectoral constraints were also noted, particularly for industries such as consumer goods and real estate, which are underrepresented due to their later adoption of ESG reporting practices.

Future studies could address these limitations by expanding the sample size, incorporating a broader range of industries, and analyzing longer time horizons. Examining market-based indicators, such as stock price volatility or valuation ratios, would offer additional perspectives on the financial impacts of ESG disclosure. Comparative analyses across developed and emerging markets could also yield insights into the global applicability of these findings. Further research could also explore the role of evolving regulatory frameworks in shaping ESG reporting practices, as well as the economic impacts of mandatory versus voluntary ESG disclosures. Additionally, examining the role of cultural and institutional factors in driving ESG adoption could provide valuable insights into regional differences in sustainability practices.