.png&w=384&q=75)

1. Introduction

Periods of macroeconomic instability – such as global financial crises, pandemics, inflationary shocks, and disruptions in global supply chains – reveal the importance of resilience within national economies. In the United States, discussions of economic stability often center on large corporations and federal policy instruments, while the role of small businesses remains underexamined, despite their widespread presence and influence.

According to the U.S. Census Bureau and the Small Business Administration, small enterprises – typically defined as firms with fewer than 500 employees – employ approximately 46% of the private workforce and account for a significant share of net new job creation. Beyond employment, small businesses contribute to the stability of local economies by circulating capital within communities, maintaining supply chain diversity, and responding flexibly to changing economic conditions. In economically vulnerable and low-density regions, they are often the primary, and sometimes only, source of goods, services, and employment.

This paper examines the financial role of small businesses as structural components of economic resilience in the United States. It posits that small firms act as decentralized stabilizers capable of absorbing and adapting to economic shocks at the community level, thereby mitigating national-level volatility. By analyzing data from recent macroeconomic disruptions and incorporating case studies from rural and economically depressed regions, this study aims to clarify how small businesses contribute to financial system stability and outline the implications for public policy and regional economic development strategies.

2. Theoretical Framework

The concept of economic resilience has gained prominence in academic and policy discourse, particularly in the context of recurrent macroeconomic shocks. Defined as the capacity of an economic system to absorb, adapt to, and recover from external disturbances, resilience is increasingly viewed not only as a function of state intervention or market scale, but also of decentralized and community-based economic structures [11, p. 71-84].

Small businesses are uniquely positioned within this framework. Their size, local embeddedness, and operational flexibility enable them to respond rapidly to shifting economic conditions, often more swiftly than larger firms constrained by hierarchical decision-making and fixed infrastructure. While large corporations may possess more capital reserves, small enterprises exhibit what some scholars term adaptive capacity – the ability to reconfigure resources, change business models, and engage with local networks to survive and even thrive during periods of disruption (Simmie & Martin, 2010).

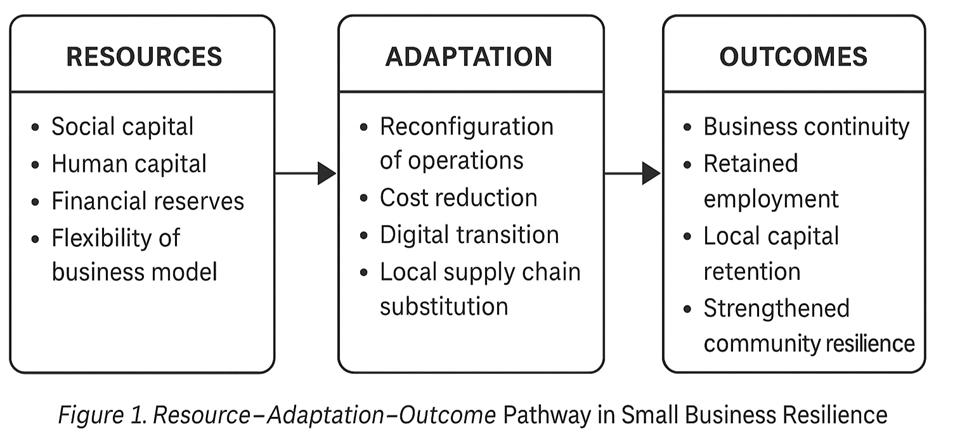

Fig. 1. Resource – Adaptation – Outcome Pathway in Small Business Resilience

This flowchart illustrates how small enterprises convert internal and community-based resources into adaptive actions that sustain local economic resilience.

Additionally, from a systems theory perspective, economic resilience is strengthened by diversity and redundancy – two characteristics inherent to an economy with a high concentration of small firms. A decentralized business landscape reduces systemic risk, as economic shocks are more likely to cascade through a monolithic supply chain or highly centralized labor structure.

Moreover, theories of localism and place-based development suggest that economies grounded in locally-owned businesses experience stronger long-term recovery trajectories due to higher capital retention, social trust, and civic engagement (Shuman, 2015). These perspectives challenge the traditional growth-centric models of economic development and emphasize the stabilizing role of small businesses, particularly in non-metropolitan areas.

This paper applies the resilience framework to assess the systemic importance of small businesses in the United States, drawing from interdisciplinary literature in regional economics, organizational theory, and public finance. In doing so, it aims to reposition small enterprises not as marginal market actors but as foundational components of economic stability in both prosperous and distressed regions.

3. Small Businesses in Times of Crisis

Small businesses have historically played a complex role in times of national and global economic crisis. While often more financially vulnerable than larger firms, they have also demonstrated significant adaptability and responsiveness during turbulent periods. This section explores how small enterprises in the United States navigated major recent crises, including the COVID-19 pandemic, inflationary pressures, and supply chain disruptions, highlighting both their fragility and their systemic resilience.

3.1. The COVID-19 Pandemic: Exposure and Adaptation

The COVID-19 pandemic posed an unprecedented challenge to the global economy. In the United States, small businesses were disproportionately affected in the initial phase of lockdowns, with many lacking the cash reserves to sustain prolonged interruptions. According to the U.S. Chamber of Commerce (2020), over 43% of small businesses reported temporary closures during the first half of 2020. However, the same crisis also revealed the sector's remarkable flexibility. Small firms quickly adopted digital tools, pivoted business models, and, in some cases, shifted product offerings entirely. For instance, local distilleries began producing hand sanitizer, and restaurants expanded into takeout, delivery, and meal kits.

The lack of capital reserves made many small businesses highly dependent on government assistance during the pandemic. Over 5.2 million small businesses applied for the Paycheck Protection Program (PPP), a federal initiative designed to provide forgivable loans to businesses in need. This large number of applications illustrates a significant vulnerability in the small business sector – without sufficient savings or liquidity, small businesses rely heavily on external financial support to survive disruptions. The reliance on such assistance underscores the fragility of small businesses in times of crisis.

Unlike large corporations, which often weather crises through capital reserves and global diversification, small businesses contribute to economic resilience through rapid operational shifts, local responsiveness, and community anchoring.

3.2. Inflation and Interest Rate Pressures

Following the pandemic, inflation surged to levels not seen in decades, driven by supply chain constraints, labor shortages, and geopolitical tensions. Small businesses, with lower pricing power and tighter profit margins, faced significant difficulties in absorbing rising costs. According to a 2022 survey by the National Federation of Independent Business (NFIB), more than 90% of small businesses experienced increased input costs, and nearly 40% raised prices in response.

This relatively low rate of price adjustments reflects a structural difference between small businesses and large corporations. While major firms – particularly in consumer goods, logistics, and technology – report passing through 80–100% of cost increases to end consumers [17], small businesses often lack the brand strength or pricing power to do so. Operating in more competitive and price-sensitive environments, they are more likely to absorb rising costs through margin compression, internal cost-cutting, or temporary losses. This resistance to inflation-driven price surges, while financially painful, contributes to economic resilience by stabilizing consumer access to essential goods and services and dampening localized inflationary pressures.

In addition to inflationary pressures, the Federal Reserve's decision to raise interest rates in 2022 further exacerbated challenges for small businesses. Over 40% of small businesses reported that the higher interest rates negatively impacted their ability to expand or take on new debt, as the cost of borrowing became more expensive. This increase in borrowing costs is another example of the financial vulnerability of small enterprises. Unlike larger corporations, which may have access to more diverse financing options and greater capital reserves, small businesses often struggle to secure favorable loans in times of economic tightening.

3.3. Supply Chain Disruptions and Local Substitution

Another key aspect of recent crises was the fragility of global supply chains. Small businesses, particularly those reliant on overseas inventory, suffered delays and shortages. Yet in some regions, these disruptions encouraged a shift toward local sourcing and production. According to a 2021 report by McKinsey & Company, local supplier networks expanded in certain sectors as small firms responded to supply volatility by forming new regional partnerships.

This reorientation not only supported business continuity but also enhanced economic resilience by shortening supply chains and increasing regional interdependence. In rural areas and small towns, where access to major distributors is often limited, small businesses filled critical gaps in essential goods and services.

3.4. Summary

In summary, while small businesses remain more financially vulnerable than large corporations – often operating with lower capital reserves, tighter margins, and more limited access to credit – they also serve as a critical source of adaptive capacity within the economy. Across recent crises, they demonstrated the ability to pivot operations quickly, absorb inflationary pressures with minimal price transmission, and reorient supply chains toward local inputs. These actions not only enabled individual business survival, but also helped stabilize local markets, preserve access to essential goods and services, and cushion regional economies from broader systemic shocks. As such, the dual role of small businesses – as both exposed and adaptive actors – positions them as key contributors to economic resilience at both community and national levels.

4. The Financial Role of Small Businesses

Small businesses do not merely participate in the economy – they shape it from the ground up, particularly in regions where larger corporations have limited reach. Their financial role extends beyond revenue generation, touching areas such as capital circulation, tax contributions, local investment multipliers, and regional stabilization.

4.1. Small Businesses as Local Economic Stabilizers

In many rural and economically distressed regions, small businesses serve as the primary source of economic stability and continuity. Their embeddedness in local communities – combined with their flexibility and personal stakeholder networks – makes them particularly important during periods of economic shock.

A study by the Federal Reserve Bank of Atlanta (2020) found that rural counties in the southeastern United States, where small businesses comprise a larger share of the business ecosystem, experienced less severe employment contraction during the early months of the COVID-19 pandemic compared to urban counties with higher concentrations of large employers. In many of these rural areas, small businesses were able to pivot more quickly – offering curbside pickup, local delivery, or transitioning services online – helping maintain at least partial economic activity despite the disruption.

Moreover, an earlier study by Goetz and Rupasingha (2009) revealed that U.S. counties with a higher density of locally owned small businesses had lower levels of economic volatility and poverty, and more consistent income growth over time. These effects persisted even after controlling for other regional characteristics, suggesting that small business presence enhances long-term resilience rather than merely short-term recovery.

These findings support the view that small businesses act as decentralized stabilizers, especially in areas where economic alternatives are limited. Their ability to preserve services, local commerce, and community employment during downturns reinforces their role as foundational elements in America’s economic infrastructure.

4.2. Circulation of Capital in Local Economies

Small businesses generate more localized economic activity than large corporations. According to a study by the American Independent Business Alliance, about 48% of each dollar spent at a local business recirculates within the community, compared to just 14% for chain retailers.

This difference is due to the local sourcing of labor, supplies, and professional services. The money spent locally tends to stay local – fueling a multiplier effect that benefits nearby households, government budgets, and other small enterprises.

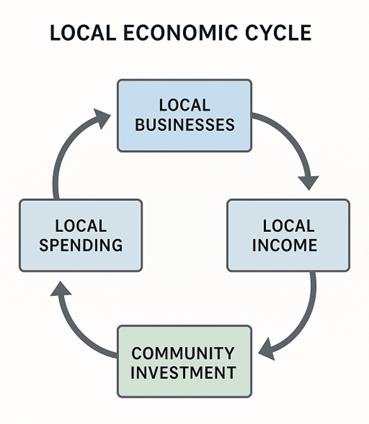

Fig. 2. Local Economic Cycle

This diagram shows how spending in local businesses circulates capital through the community, generating income, supporting reinvestment, and reinforcing regional economic resilience.

This capacity to recirculate capital locally is not just economically beneficial – it is a foundational mechanism of economic resilience. By keeping money circulating within communities, small businesses help buffer local economies against external shocks, reduce dependence on volatile global capital flows, and maintain consumption and employment even during downturns. In contrast to large firms, whose profits often exit the community, small enterprises reinforce regional self-reliance and provide a stabilizing financial infrastructure that becomes critical in times of crisis.

4.3. Employment and Tax Contributions

According to the U.S. Small Business Administration (SBA, 2022) and the U.S. Census Bureau (2023), small businesses – defined as firms with fewer than 500 employees – make up 99.9% of all U.S. businesses, and collectively employ 46.4% of the private-sector workforce, totaling over 61.7 million employees.

Their economic footprint extends beyond employment: small businesses contribute approximately 44% of the U.S. private GDP, with significant participation across industries such as construction, real estate, healthcare, and professional services. In terms of public finance, they account for nearly 40% of state and local tax revenues, including income, sales, and property taxes.

These statistics highlight the macroeconomic importance of small businesses, not only as job creators but as key fiscal contributors and engines of national productivity.

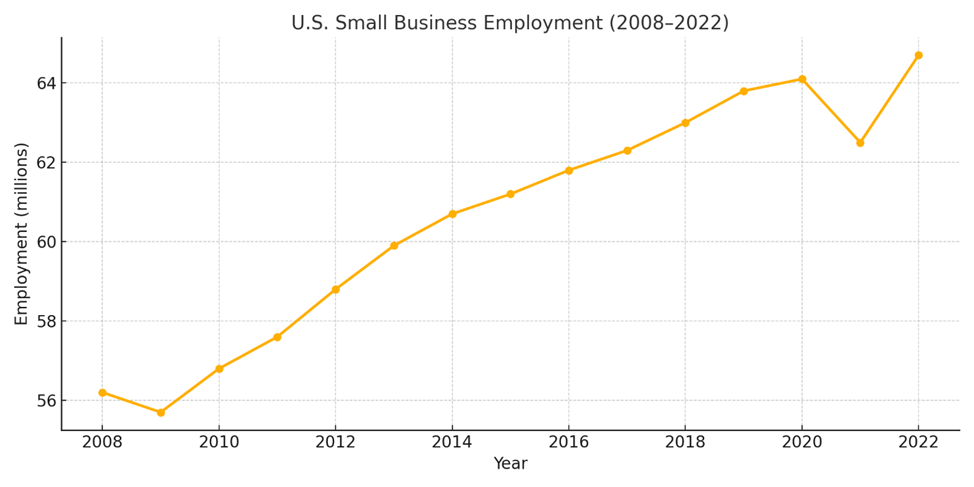

Fig. 3. U.S. Small Business Employment, 2008–2022

Employment in U.S. small businesses has shown a generally upward trend over the past 15 years, with a notable dip during the COVID-19 pandemic and subsequent recovery.

While the employment and tax footprint of small businesses may appear modest in aggregate compared to multinational corporations, their decentralized structure provides a critical hedge against systemic labor shocks. For example, the 2017 relocation of Toyota Motor North America (TMNA) from Torrance, California to Plano, Texas led to the displacement of over 2,000 corporate jobs in California and the creation of approximately 4,000 jobs in Texas, including new hires. Although the move generated an estimated $7 billion in long-term regional economic gains for the Plano area, it simultaneously disrupted the local economy of Torrance – demonstrating the risks posed by concentrated employment tied to a single large firm. In contrast, small businesses are geographically distributed and far less likely to relocate entire operations, offering greater employment continuity and tax stability at the local level. This structural dispersion acts as a form of economic shock absorption, reinforcing resilience by minimizing the risk of sudden, large-scale dislocation within regional economies.

4.4. The Multiplicative Effect of Small Business Investment

Investing in small businesses often has a broader economic impact per dollar than investing in large corporations – especially in underserved regions. A report by the Economic Policy Institute (2020) found that local small business support programs led to more sustainable job creation and higher long-term income growth when compared to tax incentives given to large companies.

For example, Startup Colorado, a state initiative, helped generate over $14 million in new capital for early-stage ventures in rural parts of the state within five years – leading not just to new businesses but to revitalized main streets and expanded local ecosystems of mentorship and supply.

4.5. Summary

Small businesses play a foundational financial role in the U.S. economy that far exceeds their scale. They act as economic stabilizers, circulate capital more locally, contribute substantial tax revenues, and produce outsized returns on public and private investment in distressed areas.

Understanding the financial role of small businesses – particularly in geographic regions neglected by larger firms – is essential to creating more inclusive, resilient, and sustainable economic policies.

These financial functions are not only economically beneficial – they represent core enablers of systemic resilience, especially in underserved regions where small businesses function as the primary economic infrastructure.

5. Case Studies and Regional Snapshots

To further illustrate the multifaceted role of small businesses in the U.S. economy, this section presents five geographically and thematically diverse case studies. These examples span rural, urban, post-crisis, and innovation-driven contexts, highlighting how small businesses adapt to regional needs while contributing to national economic goals.

5.1. Vermont – Small Business as a Driver of Local Food Economies

In Vermont, small businesses are the backbone of the state’s local food economy. According to the Vermont Sustainable Jobs Fund (VSJF, 2023) – a nonprofit organization funded by the State of Vermont – local food enterprises contribute over $11.3 billion in economic activity annually and support more than 64,000 jobs.

The Farm to Plate initiative, coordinated under state legislation (Act 54, 2009), aligns farms, food producers, distributors, and retailers into a resilient supply chain. This model demonstrates how targeted state-level policy support can help small businesses thrive while preserving regional identity and food security.

5.2. New Orleans – Post-Disaster Small Business Recovery and Urban Revitalization

Following Hurricane Katrina, small businesses played a crucial role in rebuilding New Orleans’ economic and social fabric. From 2007 to 2017, the number of small businesses in Orleans Parish increased by over 40%, as reported by the Data Center of Southeast Louisiana.

This recovery was supported by federal disaster aid (e.g., CDBG-DR) and local nonprofit accelerators like Propeller and Idea Village, which were co-funded by city initiatives and national philanthropic foundations. These efforts helped rebuild not just infrastructure but inclusive entrepreneurship ecosystems – especially in historically underserved communities.

5.3. Alaska – Small Business Innovation in Remote Economies

In Alaska’s remote and rural communities, small businesses are often the only providers of essential goods and services. According to the University of Alaska Center for Economic Development, over 73% of businesses in rural Alaska have fewer than 10 employees and serve multiple roles within communities.

Programs such as the Alaska Microloan Program (state-level) and federal support via the Denali Commission offer financial lifelines. These businesses are not just economic actors but social stabilizers, demonstrating how small enterprise can support life in geographically isolated and infrastructure-poor regions.

5.4. Colorado – Rural Tech Entrepreneurship Hubs

Rural towns in Western Colorado, such as Montrose and Durango, have seen growth in tech-enabled small businesses. Backed by programs like the Rural Technical Assistance Program and Startup Colorado–funded by state and federal partnerships–over 220 tech startups were supported between 2016 and 2022.

These initiatives provide coworking spaces, broadband access, and local investor networks. They are reversing youth outmigration and generating high-wage employment in regions traditionally reliant on resource extraction or tourism.

5.5. North Carolina – Main Street Revitalization Through Small Retail

Through the North Carolina Main Street Program, a state-administered initiative aligned with the National Main Street Center, over 2,600 small businesses were created or expanded in small-town downtown districts since 2010.

By offering grants, technical assistance, and design consulting, this program has helped communities revitalize local retail, enhance cultural tourism, and preserve architectural heritage. The initiative shows how small businesses can anchor place-based economic development and strengthen civic identity.

Summary

These case studies demonstrate the diversity of small business roles across different economic geographies in the United States–from remote Arctic towns to post-disaster cities, from food systems to high-tech hubs. Despite varied contexts, each example reveals how small enterprises serve as local anchors of stability and adaptability during times of disruption. Whether through rapid innovation, social embeddedness, or place-based reinvestment, small businesses consistently function as first responders to economic shocks. This decentralized responsiveness enhances economic resilience by distributing risk, maintaining service continuity, and accelerating regional recovery when large-scale institutions are absent, slow to respond, or structurally constrained.

6. Discussion

This analysis reinforces the view that small businesses are essential yet structurally vulnerable actors in the U.S. economy. Their outsized role in employment, regional cohesion, and innovation contrasts sharply with their limited capital reserves and exposure to macroeconomic shifts.

Compared to large corporations, which often have diversified revenue streams, access to capital markets, and internal risk buffers, small businesses typically operate with narrow margins and limited liquidity. This makes them more susceptible to external shocks, such as pandemics, inflation, or interest rate hikes. For instance, during the 2022-2023 monetary tightening cycle, over 40% of small businesses reported that Federal Reserve rate increases significantly impacted their operations. Large firms, by contrast, often benefit from fixed long-term debt, stronger banking relationships, and greater pricing power to absorb such changes.

Table 1

Resilience Profile: Small vs. Large Businesses

| Resilience Factor | Small Business | Large Business |

1 | Liquidity Reserves | Often < 3 months reserves | 6–12 months or more |

2 | Operational Flexibility | High flexibility, fast pivots | Lower (bureaucratic constraints) |

3 | Access to Credit | Limited; depends on relationship lending | Multiple financing channels |

4. | Speed of Adaptation | High (flat structure) | Slower (hierarchical decision-making) |

5. | Supply Chain Diversity | Localized or concentrated | Global, diversified supply networks |

6. | Customer Proximity | High (close to end users) | Lower (often B2B or distributed) |

This comparison highlights the structural and behavioral differences that shape how enterprises of different sizes respond to economic shocks. While large firms benefit from capital reserves and diversification, small businesses contribute to system-wide resilience through agility, community ties, and localized operations.

However, the decentralized and embedded nature of small businesses also grants them a distinctive role in economic resilience. Unlike large corporations that may relocate or downsize during downturns, small firms are frequently anchored in their communities, providing not just employment but continuity and adaptability. During the COVID-19 crisis, many small enterprises shifted quickly to delivery models, digital platforms, or new product lines–not out of strategic planning, but necessity and proximity to customer needs.

The case studies in this paper demonstrate how these businesses can serve as shock absorbers for local economies. In Vermont and Alaska, where large corporate footprints are limited, small businesses function as de facto infrastructure for food, retail, and logistics. In New Orleans, they were instrumental in post-disaster rebuilding, especially in communities that lacked attention from major investors. In Colorado and North Carolina, they are being actively positioned as engines of innovation and place-based development.

Despite their contributions, small businesses remain disadvantaged by structural gaps in financing, policy support, and infrastructure access. The widespread application for programs like the Paycheck Protection Program (PPP) underscores the fact that many lacked adequate working capital reserves or lines of credit. Moreover, many federal and state policy frameworks still treat small businesses as scaled-down versions of large firms, rather than recognizing their unique risk profiles, behavior, and developmental potential.

In sum, small businesses are not merely a complementary tier to corporate enterprise – they constitute a parallel economic architecture, one that is more localized, relational, and adaptive, yet also more exposed. Ensuring the health of this sector is not only about equity or job creation; it is central to economic resilience.

The distinctive features of small businesses–such as flexibility, local knowledge, and operational agility – contribute meaningfully to economic resilience. Table 2 summarizes how specific capabilities of small enterprises enable them to absorb and respond to economic shocks, supporting broader system stability.

Table 2

Resilience Factors and Positive Contributions of Small Businesses

| Resilience Factor | How Small Businesses Perform | Positive Impact on Economic Resilience |

1. | Operational Flexibility | High flexibility, rapid pivots in response to shocks | Maintains activity and services during crises |

2. | Speed of Adaptation | Fast reaction due to flat management structure | Quick transition to new models or markets |

3. | Customer Proximity | Close connection with customers, fast feedback loop | Improves responsiveness and social trust |

4. | Localized Supply Chains | Regional suppliers and shorter logistical chains | Reduces dependence on vulnerable global supply |

7. Conclusion

Small businesses are often celebrated for their entrepreneurial spirit and community presence, but this paper has argued that their importance goes far deeper: they are essential components of national economic structure, particularly in geographically diverse and economically vulnerable regions. According to the U.S. Small Business Administration, small enterprises account for 46.4% of private sector employment, underscoring their structural weight in the national economy.

Yet, these contributions coexist with persistent vulnerabilities. A 2022 report by the Federal Reserve found that over 50% of small businesses had less than two months of cash reserves, and more than 40% reported that rising borrowing costs due to Federal Reserve rate hikes directly impaired their growth or survival.

In sum, small businesses are not only participants in the economy but critical carriers of economic resilience. Their decentralized structure, operational flexibility, and local embeddedness allow them to act as buffers during crises–absorbing shocks, adapting services, and maintaining economic continuity. However, this role requires structural support, as resilience is not innate but developed through access to capital, policy inclusion, and entrepreneurial capacity.

Recognizing small businesses as essential components of systemic resilience is vital for policymakers, economists, and community leaders aiming to build inclusive and shock-resistant economies for the 21st century.