.png&w=384&q=75)

1. Introduction

Over the past decade, China has emerged as the world's largest e-commerce market, with online retail sales exceeding RMB 15 trillion and accounting for more than one quarter of total retail consumption. This structural shift has compelled traditional manufacturers – including those producing low-frequency, gift-oriented products such as electronic perpetual calendars – to fundamentally rethink how they design, distribute, and communicate value to consumers. Electronic perpetual calendars combine functional utility (timekeeping, weather, lunar dates) with cultural and gifting attributes, and have traditionally been distributed through offline gift wholesalers, hypermarket promotions, and corporate B2B channels. These channels, however, have shown sustained contraction since 2020 due to changes in gift culture, intensified competition from substitute products (smart speakers, smart screens), and the rapid migration of consumer attention to mobile platforms.

Against this background, the present study addresses a focal research question: How can a traditional electronic perpetual calendar company in China design and execute an e-commerce strategy that simultaneously optimizes online sales performance, marketing effectiveness, and channel architecture under conditions of digital transformation? The paper takes a representative mid-sized manufacturer (hereafter, "the Company") as a case unit, develops a strategic framework, and offers a set of recommendations that can be operationalized within a 12–18 month horizon.

The contribution of this paper is threefold. First, it consolidates the relevant literature on digital transformation and omni-channel retailing into an actionable framework tailored to a low-frequency, mid-priced traditional product category. Second, it provides empirical insight into the channel and marketing mix that best fits the Chinese consumer journey for such products. Third, it offers a sequenced implementation roadmap and key performance indicator (KPI) system that bridges strategic intent with operational execution.

2. Literature Review and Theoretical Background

2.1. Digital Transformation of Traditional Enterprises

Digital transformation refers to the use of digital technologies to fundamentally change how an enterprise creates, delivers, and captures value. For traditional manufacturers, the process typically encompasses four dimensions: customer experience, operational processes, business model, and organizational capability. Empirical research suggests that firms that integrate digital technologies across these four dimensions achieve significantly higher revenue growth and operating margins than those that pursue isolated digital initiatives. For electronic perpetual calendar producers – characterized by long product life cycles, hardware-centric R&D, and a historically B2B-oriented sales culture – the transformation challenge is particularly acute because the legacy organization is rarely structured to support consumer-facing digital operations.

2.2. E-commerce Channel Strategy

Channel strategy in the Chinese e-commerce environment has evolved from single-platform deployment toward an omni-channel architecture combining: (i) public-domain marketplaces, where Tmall and JD.com remain dominant for branded electronics; (ii) interest-based content commerce on platforms such as Douyin (TikTok China), Kuaishou, and Xiaohongshu, which combine discovery, recommendation algorithms, and live streaming; and (iii) private-domain channels – typically WeChat official accounts, mini-programs, and corporate social CRM – that reduce dependence on platform traffic costs. Recent industry studies report that brands which successfully orchestrate these three layers achieve 30–50 percent higher repurchase rates than those reliant on a single channel.

2.3. Integrated Marketing in the Social Commerce Era

The Chinese consumer journey for gift-oriented electronics is increasingly non-linear. Consumers may discover a product through short-video content, validate it through Xiaohongshu reviews, compare prices on Tmall, and finally convert through a WeChat mini-program promoted by a customer-service touchpoint. Marketing strategy must therefore shift from media-buying to integrated content production, key opinion leader (KOL) and key opinion consumer (KOC) collaboration, and continuous engagement throughout the lifecycle. Theoretical frameworks such as the AIPL model (Awareness–Interest–Purchase–Loyalty) and the FAST model (Fertility, Activity, Superiority, Total fans) have been widely adopted by Chinese e-commerce operators to operationalize this perspective.

3. Methodology

The research adopts a qualitative single-case study design supplemented by secondary market data. Data collection comprised: (a) semi-structured interviews with management, sales, and marketing personnel of the Company; (b) analysis of internal sales and channel performance data from 2022 to 2025; (c) review of competitor public disclosures and platform reports from Alibaba, JD.com, and ByteDance; and (d) consumer journey mapping based on online review mining from Tmall, JD.com, and Xiaohongshu. The strategic framework synthesizes these inputs through a SWOT analysis, channel diagnostic, and a four-phase planning model. The methodology is appropriate for exploratory research aimed at producing actionable, context-rich recommendations rather than statistically generalizable findings.

4. Industry and Company Diagnosis

4.1. Market Overview of Electronic Perpetual Calendars in China

The electronic perpetual calendar category in China comprises three principal segments: entry-level functional units (RMB 80–200), mid-range gift-oriented models with weather and lunar features (RMB 200–600), and premium designer or smart-screen variants (RMB 600+). The total category retail value is estimated at RMB 4.5–6 billion annually, with single-digit growth in unit terms but a clear upward shift in average selling price driven by premiumization and gifting demand. Online channels currently account for approximately 55–60 percent of category sales, up from less than 30 percent five years earlier.

4.2. SWOT Analysis of the Focal Company

Table 1 summarizes the SWOT diagnosis of the Company.

Table 1

SWOT Analysis of the Focal Company

Strengths | Weaknesses | Opportunities | Threats |

|

|

|

|

The diagnosis reveals a classic asymmetry: the Company possesses meaningful manufacturing strengths but lacks the digital-native capabilities required to convert these advantages into consumer-facing market share. The strategic priority is therefore to build digital capability rapidly while leveraging existing supply chain advantages to compete on quality and reliability rather than price.

4.3. Existing Channel Performance

Table 2 presents a simplified breakdown of the Company's current sales by channel and the strategic intent for each. The current channel mix is heavily skewed toward offline distribution (approximately 62 percent of revenue), while online sales remain concentrated on a single Tmall flagship store with limited content investment.

Table 2

Current and Target Channel Mix of the Focal Company

Channel | Current Share | Target Share (3 yrs) | Strategic Role |

Offline distributors (B2B) | 62% | 35% | Maintain core gifting and corporate procurement business; rationalize underperforming dealers. |

Tmall flagship store | 18% | 22% | Brand image hub; focus on premium SKUs, ratings, and search dominance for category keywords. |

JD.com flagship store | 8% | 13% | Logistics-driven trust play; emphasize after-sales and 3C-buyer demographic. |

Douyin/TikTok Shop | 5% | 15% | Discovery and impulse-purchase engine; live streaming + short video content. |

Xiaohongshu (RedNote) | 2% | 5% | Female / gifting reviews and aesthetic positioning; KOC seeding. |

WeChat mini-program (private domain) | 3% | 8% | Member retention, repurchase, and corporate group-buy gifting orders. |

Cross-border e-commerce | 2% | 2% | Test-and-learn for Southeast Asia and the Middle East via TikTok Shop and Lazada. |

5. Strategic Framework and Roadmap

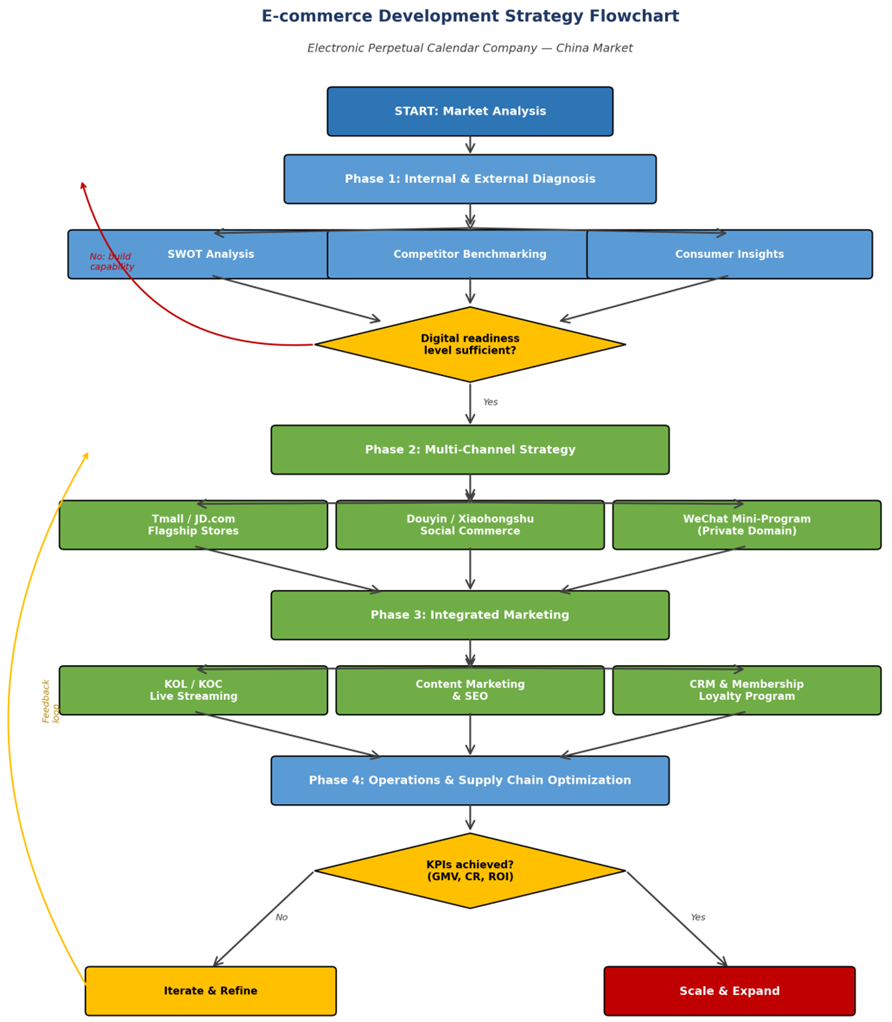

Building on the diagnosis, the paper proposes a four-phase strategic framework, illustrated in Figure. The framework moves the Company from internal diagnosis through channel and marketing redesign to operational and supply-chain alignment, with a feedback loop that institutionalizes continuous optimization based on performance data.

Fig. Strategic Framework for E-commerce Development of an Electronic Perpetual Calendar Company in China

5.1. Phase 1 – Internal and External Diagnosis

Phase 1 institutionalizes a quarterly diagnostic cycle covering competitor benchmarking, consumer review mining, and internal capability assessment. Key outputs include a refreshed SWOT, a digital readiness scorecard, and a prioritized capability gap list. A formal go/no-go gate determines whether the organization possesses the minimum capabilities (data infrastructure, content team, e-commerce operators) to scale the strategy. If not, capability building precedes scale-up.

5.2. Phase 2 – Multi-Channel Architecture

Phase 2 redesigns the channel architecture along three layers. The public-domain layer (Tmall, JD.com) anchors brand image, search dominance, and price benchmarks. The content-commerce layer (Douyin, Xiaohongshu) drives discovery, interest, and impulse purchase among younger and female consumers, particularly during festival and gifting periods. The private-domain layer (WeChat official account, mini-program, social CRM) captures and retains customers, supports repurchase, and unlocks corporate group-buy revenue. A unified product-information management (PIM) system ensures consistent SKU, pricing, and content across channels, while a tiered SKU strategy avoids direct cross-channel price conflicts.

5.3. Phase 3 – Integrated Marketing

Phase 3 operationalizes a content-led marketing engine. The recommended marketing mix is summarized in Table 3, organized around the AIPL consumer journey.

Table 3

Integrated Marketing Mix Mapped to the AIPL Consumer Journey

Stage | Primary Channels | Tactics | KPIs |

Awareness | Douyin short video, Xiaohongshu, WeChat Channels | Brand storytelling, festival campaigns, KOL seeding | Reach, video views, brand search index |

Interest | Xiaohongshu, Douyin live, Tmall product pages | KOC reviews, demonstration videos, comparison content | Engagement rate, store visits, add-to-cart rate |

Purchase | Tmall, JD.com, Douyin Shop, mini-program | Live-stream selling, festival promotions, bundling, coupons | GMV, conversion rate, AOV, ROI on paid traffic |

Loyalty | WeChat mini-program, official account, member CRM | Tiered membership, exclusive new-product launch, referral rewards, B2B group-buy | Repurchase rate, NPS, CLV, member GMV share |

Particular emphasis is placed on live streaming, which has become the most efficient single conversion mechanism for gift-oriented electronic products in China. The Company should invest in a self-operated live-streaming studio, complemented by a long-tail network of mid-tier KOLs and KOCs, while reserving top-tier celebrity collaborations for major festival peaks (Double 11, 618, Spring Festival, and Mid-Autumn Festival).

5.4. Phase 4 – Operations and Supply Chain Optimization

The shift from B2B distribution to direct-to-consumer e-commerce imposes new operational requirements: SKU proliferation, smaller and more frequent order batches, faster delivery expectations, and higher reverse-logistics volumes. The Company should establish: (i) an integrated order management system connecting all channels; (ii) regional warehousing arrangements with third-party logistics partners to compress delivery to within 48 hours nationwide; (iii) a dedicated after-sales team for online customer service with same-day response targets; and (iv) a demand-sensing process that uses live-stream and platform data as leading indicators for production planning.

6. Implementation Roadmap and KPIs

Implementation is sequenced over 18 months, with explicit KPIs assigned to each phase. Table 4 summarizes the roadmap.

Table 4

18-Month Implementation Roadmap and KPIs

Period | Strategic Focus | Key Initiatives | Target KPIs |

Months 1–3 | Foundation | Diagnostic completion, organizational redesign, recruitment of e-commerce and content teams, PIM system selection | Team in place; data infrastructure live; content backlog of 100+ assets |

Months 4–9 | Channel build-out | Tmall flagship upgrade, JD store launch, Douyin Shop opening, Xiaohongshu seeding, mini-program v1 | Online revenue share +10pp; Tmall search share top-3 in category |

Months 10–14 | Marketing scale-up | Self-operated live streaming, KOL/KOC matrix, festival campaigns, B2B group-buy program | ROI ≥ 1:4 on paid traffic; live-stream GMV ≥ 20% of online GMV |

Months 15–18 | Optimization & expansion | Cross-border pilot, premium product line launch, full omni-channel data integration | Repurchase rate ≥ 18%; cross-border revenue ≥ 5% of total |

7. Risks and Mitigation

Three principal risks must be actively managed. First, channel conflict between online flagship stores and offline distributors can erode dealer trust; mitigation requires differentiated SKU strategies, exclusive online editions, and transparent pricing governance. Second, traffic-cost inflation on major platforms can compress margins; mitigation depends on building private-domain assets, lifting average order value through bundling and gift-set design, and improving organic search and content rankings. Third, organizational resistance to digital transformation is common in established manufacturing firms; mitigation involves CEO-level sponsorship, clear KPI alignment, dedicated digital P&L responsibility, and partial use of external agency support during the build phase.

8. Conclusion

Digital transformation is no longer optional for traditional electronic perpetual calendar producers in China. The findings of this study indicate that a structured four-phase framework – diagnosis, multi-channel architecture, integrated marketing, and operational alignment – supported by clear KPIs and a realistic 18-month roadmap, can shift a traditional manufacturer from offline-dependent distribution to a balanced omni-channel model. The most important strategic levers are the orchestration of public-domain marketplaces, content commerce, and private-domain operations under a unified data and brand strategy; the institutionalization of content-led integrated marketing along the AIPL journey; and the rebuilding of operations and supply chain capability to serve a direct-to-consumer business. While the case-study methodology limits statistical generalization, the framework is portable to other low-frequency, gift-oriented hardware categories facing similar transformation pressures. Future research should test the framework across multiple firms and over a longer horizon, and quantify the relative contribution of each strategic lever to financial performance.

.png&w=640&q=75)